Special finance events for Dubai & Abu Dhabi OFWs!

By Randell Tiongson on August 18th, 2015

I will be back in the UAE for a series of training for the OFWs this September! It’s time to level up learning and be on your way to financial peace!

1) Economics 101 & Investment Outlook (Dubai) — this program will discuss the rudiments of economics especially matters that will have an effect to investors. How does interest affect investments? How does inflation play a factor in growing your wealth? How does monetary policies used to spur the economy?The program will touch up on basic macroeconomic learning as well as a thorough look on the Philippine economy as a bonus feature of the event. It is high time that we all understand economics and how it affects our everyday lives!

To register, click HERE or email dubaifinancialevents@gmail.com

2) Retirement & Estate Planning (Abu Dhabi)

Studies shows that only 1 to 2 out of 10 Filipinos prepare for retirement. Studies also reveals that the few who prepare for retirement, most of them will only exhaust their retirement funds halfway through retirement. Filipinos are experiencing longer life expectancy but unfortunately, huge costs are needed to live a life of comfort during those years.

Consider this: If you can generate 75% of your pre-retirement income during your retirement years, you will live a life of comfort; if you can only generate 30-50%, you will live a life of struggle. For a 20 year retirement, you need at least 20 years of preparation — if you plan to retire at 60, then you should start preparing at 40.

As and added feature, I will also discuss basics of estate planning under the Philippine setting. Many Filipinos are unaware of why estate planning is important to them.

To register, click HERE or email dubaifinancialevents@gmail.com

HURRY! We are only limiting this offerings through limited slots only.

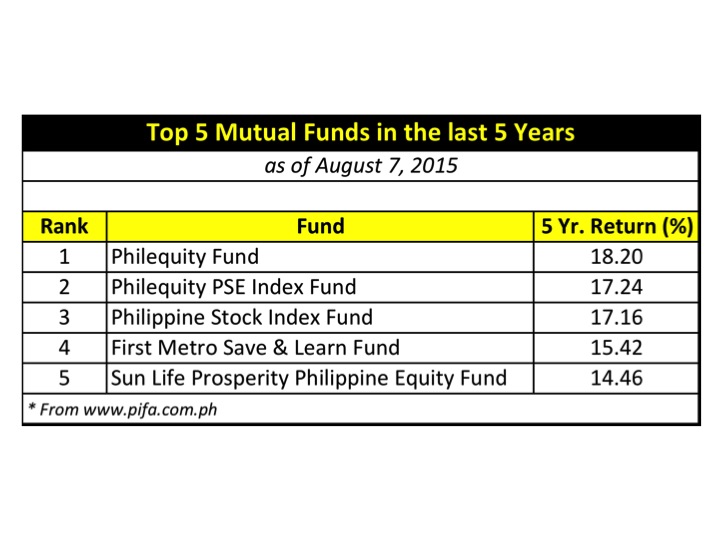

Top 5 mutual funds in the last 5 years

By Randell Tiongson on August 10th, 2015

There has been a lot of anxiety with what’s happening in the equities market. External forces have affected the local bourse and many investors are jittery. China, Greece and a slowing down of the economy has largely contributed to some declines lately.

The equities market are behaving the way it is supposed to behave, it goes up and down and it is largely sentiment driven. How about mutual funds? Are the fund managers doing their jobs in ensuring growth in their funds despite the volatility?

I recently checked out how the mutual funds are doing and I am happy to note that while the short term gains are very minimal, even losses for some funds, many funds are doing admirably when you look at them from a long term perspective… say 5 years. I have always subscribed to the belief that investing in the stock market is more about time and less about timing — time in the market is better than timing the market. Of course many traders will disagree but my purpose of going into the equities market has always been from an investors perspective and not of a trader.

When investing in pooled funds like mutual funds or UITF, it is best that you do so with a long term perspective — the longer you stay, the better it is! I recommend that you stay invested in your funds for as long as you can, and you only redeem them when you have already hit your objective. It is always best to know what your investment objectives are, as well as your time frame and risk tolerance. Once you have established them and invested your money, don’t react too much with how the market moves and always view your investments from a long term perspective. It will make you less jittery and it will keep you sane, trust me!

Below is a summary of the top 5 mutual funds in the last 5 years. Always remember, however, that past performance is not an indication of future performance — today’s top performer can be tomorrow’s laggard. A strategy I use is peso cost averaging — I invest in a monthly basis regardless of where the market is. But, whenever the market dips and I have investible funds, I try to buy more. It may not be the best strategy but it is a strategy that works for me. Of course, always remember to diversify your investments.

Happy investing!

Do we really need car insurance?

By Randell Tiongson on August 8th, 2015

Question: My wife and I just bought our first car and we need help choosing the right car insurance. Is the basic CPTL insurance offered by the LTO enough? Or is it worth buying a comprehensive car insurance? If we choose the latter, what are the things we should be looking out for? –John Santos via Facebook

Answer: Congratulations on the new car! It’s natural to feel unsure and overwhelmed when buying car insurance for the first time. Let me guide you through the process.

When you register your car with the Land Transportation Office, you are required by law to get basic Compulsory Third Party Liability (CTPL) car insurance to protect against possible liabilities to third parties. According to the Insurance Code of the Philippines, a third party is defined as any person other than a passenger, family member, or household member of the vehicle owner.

When you register your car with the Land Transportation Office, you are required by law to get basic Compulsory Third Party Liability (CTPL) car insurance to protect against possible liabilities to third parties. According to the Insurance Code of the Philippines, a third party is defined as any person other than a passenger, family member, or household member of the vehicle owner.

In other words, CTPL protects pedestrians from potential damages or injuries that arise from the use of the insured car. This is compulsory and covers any bodily injuries or deaths caused for of up to P100,000. However, CTPL does not cover loss or damages to property, and is very limited in this regard.

Many non-life insurance providers also provide comprehensive car insurance. Essentially, comprehensive car insurance has a wide coverage and insures you against damage, car theft, liabilities caused by collisions, fire, malicious acts, acts of God (and nature) and personal accident insurance of the passenger. While this is not mandatory, it provides some measure of financial security by covering car repairs and other damages should any unfortunate incidents occur.

It’s smart to get this type of insurance because risk is an everyday reality. Accidents can happen to you anytime, and if you’re driving to work every day, you’re exposed to risks that you do not have direct control of.

To illustrate, EDSA accommodates more than two million vehicles on a daily basis. If you take Edsa to work, you’re exposed to more than 27,000 public utility buses that figure in the worst traffic accidents.

Another good reason to get comprehensive car insurance is the fact that the Philippines endures an average of nine tropical storms in a year. It’s like saying your car is at major risk at least nine times in a year! I have a lot of friends who had damaged cars during the worst flooding in Manila. Those who had Acts of God or Acts of Nature in their policy were well-taken care of by their insurance providers.

If any of these unfortunate incidents makes your car inoperable, comprehensive insurance picks up the tab for repairs and does all the legwork for you. So instead of doing the paperwork and trying to get them stamped at one government office after another, the insurance company will take care of all this. Depending on your coverage, they’ll even foot the hospital bills in case any passengers got injured in the accident.

When getting your car insurance, make sure that you read the fine print and understand what’s included and what isn’t. Many “comprehensive” insurance policies don’t insure against all types of damages, like riots or typhoons. Coverage for these instances will require additional clauses:

Acts of God or Acts of Nature covers damage from flooding and other non-manmade incidents

Personal Accident provides a small amount for any injuries sustained during a road accident

Medical Reimbursement lets you reimburse medical expenses from injuries related to the accident

Other add-ons include riot (for protest or riot-related damage), upgrade (for upgraded car equipment), roadside repairs and towing

Before including these add-ons to your coverage, determine how and where you use your car. For example, if you live in a flood-prone neighborhood, the Acts of God clause is worth paying for. If you drive to work daily, it’s safe to include the Personal Accident or Medical Reimbursement additions.

Get to know the top car insurance providers in the Philippines and see what coverage they have to offer. As a shortcut to your research, there are several websites offering comparisons among the car insurance packages of various providers. A good comparative website you can use is Moneymax.

These websites will give you quotes from four or more companies, and do a side-by-side comparison. This makes it easier for you to analyze your options and make your choice based on price and your own needs.

Make sure that you compare premiums fairly and objectively before making your final choice. Some insurance companies may offer very low rates, but the claiming process can be difficult.

Ask your friends which providers they are using and find out how easy or difficult the claims process was. Personally, I don’t mind paying a few pesos more if my insurance provider rescues me during my time of need.

Be safe, be secured.