My new book, BLUE CHIP: A No Nonsense Guide to Raising Financially Smart Kids, is now available for order.

This is a book I felt the need to write for some time, and I believe the timing is right. Many parents want to teach their children about money, but often do not know where or how to begin. We teach our children many important things in life, but sometimes we forget that financial wisdom is also part of formation.

Here is a short snippet from the book:

“Raising financially smart kids is not just about teaching them how to save money. It is about shaping their hearts, forming their character, and helping them understand that money is a tool to be managed wisely, not a master to be served blindly.”

That is really the heart of BLUE CHIP.

This book was written to help parents raise children who are not only financially smart, but also wise, responsible, generous, and grounded in the right values.

It is applicable to parents with children of all ages. Whether your kids are still young, already in school, entering college, starting work, or even building their own families, there are principles here that can help guide meaningful conversations and practical lessons on earning, spending, saving, giving, stewardship, contentment, and generosity.

I believe this can help many parents because financial lessons are best learned at home. Our children are always watching how we spend, save, give, borrow, work, and respond to lack or abundance. BLUE CHIP is designed to help parents become more intentional in those everyday moments, turning ordinary money conversations into opportunities for discipleship and life formation.

The book is only P500.

A Small Group Study Guide is also available for only P150, useful for discussions among parents, couples, families, and small groups who want to process the lessons together.

For this initial sale, the Study Guide will be FREE for every purchase of the book.

Delivery fee: P100 for Metro Manila orders P160 for provincial orders

This special offer with the free Study Guide ends on June 15, 2026.

My prayer is that BLUE CHIP will help many families begin the right conversations at home, because raising financially smart kids is not just about money. It is about character, wisdom, stewardship, and preparing the next generation to live with purpose and generosity.

To place your order:

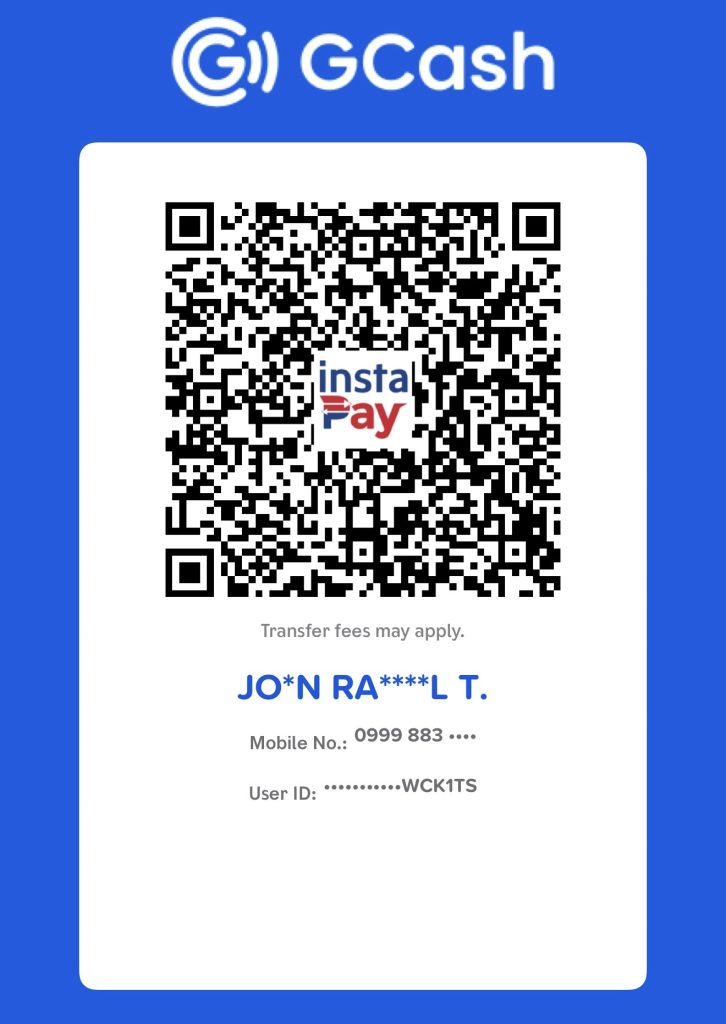

Send payment to BDO #008868001849 or BPI #0249111309 or GCash 09998837273 (or QR)

Take a screenshot of the deposit slip or transfer advise

Send an e-mail to michaelenero6@gmail.com along with the payment advise, your complete address and contact number.

GCash QR Code

Let’s all raise the next generation of financially smart kids!

Tithing While in Debt: Faith, Wisdom, and a Generous Heart

By Randell Tiongson on May 16th, 2026

One of the questions I often hear from people who are trying to fix their finances is this: “Should I still tithe while I am in debt?”

It is a very honest question and I believe it deserves a honest, biblical, and practical answer.

For many believers, tithing is a deeply held conviction. It is a way of honoring God, acknowledging that everything we have comes from Him, and participating in kingdom work. I respect that deeply and I also believe that giving is an important part of discipleship because money has a way of revealing what is happening in our hearts.

But I also believe we need to approach this question with both faith and wisdom.

And here is my personal take: if you are drowning in consumer debt, it may be okay to pause on tithing for a season, focus on becoming debt-free, and then resume giving with greater freedom, joy, and generosity.

I know that may sound controversial to some, but allow me to explain.

When a person is buried in credit card debt, personal loans, or other high-interest obligations, the money being used is not really “extra” money, in many cases, it is borrowed money. So mathematically and ethically, it may be more practical and responsible to prioritize paying back what is owed. Romans 13:8 says, “Owe no one anything, except to love each other…” While this does not mean every kind of borrowing is automatically sinful, it does remind us that debt is a serious obligation. When we borrow, we make a commitment to repay and that commitment must be treated with integrity.

This is why I believe there is wisdom in saying, “Lord, I want to honor You with my money, and part of honoring You right now is getting out of debt, paying what I owe, and learning to live within my means.” That, to me, is not a rejection of generosity. In many cases, it is preparation for greater generosity.

Now, let me be clear, I am not saying people in debt should stop being generous altogether. Generosity is not limited to money. Even in difficult financial seasons, we can still give encouragement, time, service, hospitality, prayer, and care. We can still live with an open heart, we can still resist selfishness, we can still say, “Lord, form me into a generous person.”

The issue is not whether we should be generous. As followers of Christ, generosity is part of who we should be becoming. The issue is whether someone who is financially overextended should continue giving a fixed percentage while struggling to meet obligations, pay creditors, provide for family, or escape the cycle of debt. In those situations, I believe wisdom is needed.

There are also exceptions as not all debt is the same. A home mortgage or a car loan, for example, may be structured over many years and can be properly programmed into a household budget. These are different from uncontrolled credit card debt or loans used to fund a lifestyle we cannot afford. Long-term debt, when managed responsibly and within one’s capacity, should not require a pause in tithing or giving.

But if the debt is toxic, high-interest, and already creating stress, anxiety, and financial instability, then the priority may need to be debt freedom.

I often say that faith and wisdom are not opposed to each other. In fact, biblical faith should produce wise living. Faith is not recklessness and wisdom is not unbelief.

Proverbs 22:7 reminds us, “The borrower is the slave of the lender.” Debt can limit our options, affect our peace, strain our relationships, and even reduce our capacity to give. So when we pursue debt freedom, we are not merely trying to improve our financial position, we are also trying to regain freedom so we can live more faithfully, peacefully, and generously.

At the same time, I want to be careful not to turn this into a rigid rule. This is where conviction comes in. Some people may feel strongly convicted to continue tithing even while paying off debt. If they can do so with faith, wisdom, and without neglecting their obligations, then I honor that. God works in people’s hearts differently, and there are many testimonies of people who continued giving during difficult seasons and experienced God’s provision in powerful ways. But others may feel convicted that the most faithful thing to do is to pause their tithe temporarily, aggressively pay off debt, and then return to giving with a freer heart. I believe that can also be a valid and responsible path.

The key word here is temporarily.

Pausing tithing should not become an excuse for selfishness. It should not become a way to avoid generosity permanently. It should be part of a clear plan: reduce expenses, stop borrowing, pay debts, rebuild financial stability, and grow into a life of generosity, tithing, and beyond. Because the goal is not simply to become debt-free. The goal is to become free to obey God more fully. A debt-free life gives us more margin to support the work of the kingdom, help people in need, bless our families, and give without resentment or fear. For me, that is the bigger picture.

So, what should you do if you are in debt?

First, be honest about your financial situation. Do not spiritualize poor money management and face the numbers.

Second, pray and seek counsel. Talk to mature believers, leaders, or trusted financial mentors who can help you process both the spiritual and practical sides.

Third, make a debt payment plan. Stop adding new debt, cut unnecessary expenses, increase income where possible, be intentional.

Fourth, keep your heart generous. Even if you pause tithing for a season, do not pause discipleship, do not pause gratitude and do not pause compassion.

Lastly, aim to resume giving as soon as you are able. Better yet, grow toward a life that is not just about tithing, but about generosity beyond the tithe.

At the end of the day, God is not after our money first, He is after our hearts. Tithing is important, but it is not meant to be separated from wisdom, integrity, responsibility, and love. Paying our debts is also an act of faithfulness. Living generously is also an act of worship. Managing money wisely is also part of discipleship.

So if you are in debt today, do not live under condemnation. Take responsibility, make wise decisions, and trust God in the process. The Lord is not only concerned about what you give, He is also forming the kind of person you are becoming.

And my prayer is that as we grow in financial wisdom, we will also grow in freedom, peace, and generosity. Not just tithing, but tithing and beyond.

Low Growth, High Inflation, and the Filipino Squeeze

By Randell Tiongson on May 11th, 2026

The Philippine economy is in a precarious situation, and I do not think we should sugarcoat it.

We are facing a difficult combination: low economic growth, high inflation, a weak peso, and deep import dependence. That is a painful mix for any economy, but especially for a country like the Philippines where many households already live with very little financial margin.

When GDP growth is weak, incomes and job opportunities do not expand fast enough. But when inflation is high, the cost of living continues to rise, so families are squeezed from both sides… their income does not grow fast enough, while their expenses keep increasing.

That is not just an economic statistic, that is the reality of parents trying to stretch grocery budgets, workers dealing with higher commuting costs, small businesses absorbing higher input prices, and households postponing important needs because their money simply does not go as far as before.

One of the biggest reasons we are vulnerable is that the Philippines remains a net importer of so many things. We import much of our energy, fuel, food products, raw materials, machinery, industrial inputs, and even many consumer goods. This makes us extremely exposed whenever global prices rise, supply chains are disrupted, oil prices spike, or the peso weakens.

A weak peso does not stay in the financial markets. It eventually shows up in the price of fuel, food, electricity, transportation, and business costs. Since many imported goods and inputs are priced in dollars, a weaker peso means we pay more in local currency for the same products. Businesses eventually pass those costs on to consumers, and ordinary Filipinos carry the burden.

This is why inflation in the Philippines is not merely a monetary issue, it is also a structural issue.

Yes, monetary policy matters. The Bangko Sentral ng Pilipinas can raise or lower interest rates, it can manage liquidity, anchor inflation expectations, and help stabilize the currency. These are important tools. Monetary policy can help smoothen the edges of volatility.

However, monetary policy cannot plant rice, it cannot produce oil, it cannot build cold storage facilities, it cannot build roads, it cannot fix ports, it cannot solve agricultural productivity, it cannot create deep manufacturing capacity, it cannot reduce our dependence on imported fuel and it cannot substitute for serious government policy and fiscal reform.

This is where we need to be more honest as a nation. If growth is low and inflation is high, then simply adjusting interest rates will not be enough. High interest rates may help control inflation, but they can also slow down borrowing, investment, and consumption. Lower interest rates may help stimulate growth, but if the real problem is supply, imports, energy dependence, and weak productivity, then lower rates may not solve the deeper problem either. In other words, we cannot interest-rate our way out of structural weakness.

The deeper issue is that we do not produce enough of what we need. We consume far more than we create domestically. We rely heavily on imports, remittances, consumption, and services. These are strengths in some ways, but they are not enough to build a resilient economy.

We need real structural economic reforms.

We need to strengthen agriculture, not only through subsidies, but through productivity, irrigation, mechanization, farm consolidation where appropriate, better logistics, cold-chain systems, post-harvest facilities, and direct market access. Food security cannot remain a slogan, it must become a serious national priority.

We need a long-term energy strategy. A country that imports most of its fuel will always be exposed to global shocks. We need a diversified, reliable, and affordable energy mix. Renewable energy should be accelerated, but reliability and cost must also be addressed. Energy policy cannot be driven only by political cycles, it must be treated as a generational issue.

We need to build manufacturing and industrial capacity. Not protectionism for its own sake, but strategic value creation. We need to ask: What can the Philippines produce competitively? What industries can create quality jobs? What sectors can reduce import dependence? Where can we build scale? Where can we become globally relevant?

We also need fiscal policy that is disciplined, targeted, and developmental. Government spending must build capacity, not merely visibility. Infrastructure must lower the cost of doing business. Education spending must improve skills. Agricultural spending must increase productivity. Social protection must protect the vulnerable without creating permanent dependency. Fiscal policy must be about nation-building, not just budget utilization.

This is also a governance issue. Investors look beyond interest rates, they look at policy consistency, corruption risks, infrastructure quality, ease of doing business, rule of law, and institutional credibility. A country may have talented people and strong potential, but weak systems will always limit progress. The danger is that we keep treating symptoms while avoiding the disease.

High inflation is a symptom, weak domestic production is a deeper issue. A weak peso is a symptom, heavy import dependence is a deeper issue. Low GDP growth is a symptom, weak productivity, low investment, and poor execution are deeper issues.

For ordinary Filipinos, the response must still be prudence, build emergency funds, avoid unnecessary debt, be careful with lifestyle inflation, increase skills and diversify income where possible. Understand that inflation and currency weakness will affect the household budget.

But personal discipline must be matched by national discipline. Filipinos cannot budget their way out of a structurally weak economy. Households can adjust, but government must reform. Families can tighten belts, but policymakers must build capacity. Businesses can innovate, but the country must create an environment where enterprise can thrive.

The Philippines has great potential, I still believe that. We have a young population, talented workers, a strategic location, and a large domestic market. But potential is not the same as progress, potential must be stewarded.

And that is the word I keep coming back to: stewardship. A nation’s economy is also a stewardship issue. We must manage resources wisely, make courageous decisions, and think beyond the next election cycle. We cannot simply consume what others produce, import what we fail to develop, borrow what we cannot afford, and hope that monetary policy will rescue us every time.

Low GDP growth, high inflation, a weak peso, and import dependence are not isolated problems. They are connected warning signs. They are telling us that we need to build a stronger, more productive, more resilient Philippine economy.

We do not need cosmetic solutions, we need structural reform, we need courageous leadership, wise policy, disciplined execution, and long-term thinking. But as we call for these things, we must also remember that behind every economic statistic is a person, a family, a worker, a parent, a business owner, and a community trying to endure.

This is why our response must not be fear, anger, or despair. It must be wisdom, compassion, and faithful stewardship.

From a kingdom perspective, economics is never just about money, markets, or numbers. It is about people, justice, work, provision, generosity, and the faithful stewardship of what God has entrusted to us. The kingdom of God reorders the way we see resources. We do not see wealth merely as something to accumulate, but as something to steward. We do not see work merely as a way to survive, but as a calling to create value. We do not see policy merely as technical governance, but as a responsibility to pursue justice, protect the vulnerable, and promote human flourishing.

For households, this means learning to live wisely, avoid unnecessary debt, build emergency funds, increase skills, and make thoughtful financial decisions. For business owners, it means creating value, treating people fairly, and building redemptive enterprises that serve more than profit. For leaders, it means making decisions not merely for political survival, but for the good of the next generation.

And for all of us, it means remembering that while we live in the world’s economy, we are called to follow a different set of priorities. The world’s economy often teaches fear, scarcity, greed, and self-preservation. The kingdom teaches trust, wisdom, generosity, justice, and stewardship.

We can be prudent without being anxious. We can be realistic without becoming hopeless. We can prepare responsibly while still trusting that God remains faithful in uncertain times.

The economy may be fragile, but our hope does not have to be.

God calls us to steward what is in our hands, care for those who are vulnerable, speak truth where reform is needed, and keep building even when the times are difficult. Kingdom people do not ignore economic realities… we engage them with wisdom, courage, and compassion because we know that God cares about the poor, the worker, the family, the marketplace, and the future of the nation.

Because in the end, the real question is not only how we survive the next oil price shock, inflation spike, or currency movement. The bigger question is this:

Are we building an economy, a society, and a way of life that reflects God’s justice, blesses the vulnerable, rewards honest work, and serves the next generation of Filipinos?

May God give us the wisdom to reform what must be reformed, the courage to lead where leadership is needed, and the grace to remain faithful in the work entrusted to us. Most importantly, may we humble ourselves before the Lord and acknowledge that our ultimate savior is Jesus Christ.

Want to learn how to manage your finances better?

Register now and get a free copy of my e-book. Start your financial planning journey today!