Where should I invest? Mutual funds, UITF, VUL or stocks?

By Randell Tiongson on September 1st, 2015

Question: HI, I’ve recently decided to start investing, but I don’t know which product I should choose. Should I invest in variable universal life insurance, a mutual fund, UITF or buy stocks? —Asked by Josiah via Facebook

Answer: First of all, congratulations on taking this important step in your journey to financial peace! But the question of which product is right for you depends on where you are in life and what your goals are. While I can’t make any specific recommendation because I don’t know more about your financial situation, I can give you a broad overview of each product you mentioned to help you make the right decision.

I’m an advocate of life insurance, which is something Filipinos sorely lack. Variable life insurance (or VUL) is a product you can consider if you need both insurance and investment. VUL will give you insurance benefits but it will also have a fund that is being invested according to your objectives, risk profile and other preferences. If there are already people depending on your income, you should get a life insurance policy. But if your sole objective is purely investing, then this may not be the right instrument for you at this time, because in the first couple of years of your policy, most of your money will actually go toward premium payments.

If what you want is to put all your money in investments, and your risk tolerance is moderate to high, UITFs and mutual funds can work for you. A big advantage of these is that they are professionally managed by experienced investment managers, who are trained to invest properly. Even if you yourself are not well-versed in investing, you can rest assured that you’re in good hands.

The main difference between these two is that UITFs are offered by banks, while mutual funds are their own companies. By buying into a UITF, you own units of this fund. By buying into a mutual fund, you own shares and become a shareholder in the mutual fund company. All your earnings are net of tax and fees as represented by the NAVpu (net asset value per unit) for UITFs and NAVps (net asset value per share) for mutual funds.

When it comes to these pooled funds, you can choose from a variety of investments for every risk appetite. You can also choose among actively managed funds, where a fund manager tries to beat the index, or passively managed funds, which simply try to match the performance of an index.

In more economically advanced countries, passively managed funds match or outdo the performance of actively managed funds because those markets are already efficient. However, in younger markets like in the Philippines, active fund managers can still perform better than the index because the market is not efficient yet and there are still advantages they can leverage.

However, investing in mutual funds and UITFs comes with some disadvantages. The management costs can be significant, going to up to 2 percent. For UITFs, sometimes the bank branch staff aren’t trained to handle inquiries, and some of them might even discourage you.

Mutual funds and UITFs will work for you if you don’t need the money right away and can stand risk, but don’t have the time to learn all about stocks. They’re also a good vehicle for retirement funds because the long-term nature of your need will allow you to weather the fluctuations of the market. I’m encouraged by the good performance of many funds over the last few years, but keep in mind that past performance is never an indication of future performance.

Now we come to the elephant in the room: stock investing.

Individual stocks come with a lot of advantages: you have direct control over what you buy, unlike in a pooled fund that is automatically diversified. You get residual income if you buy a stock which pays out good dividends. Your returns are maximized because you’re not paying management fees, and if your individual stock outdoes the market, you make money even if the market as a whole is going down. And if you choose the right balance of stocks, your portfolio’s growth can outperform the index.

But! Before you start counting your chickens, know that stock investing is not easy to get into. You’re going to have to spend a lot of time learning about how it works. You’ll also have to learn fundamental and technical analysis, spending time reading financial reports from the companies you want to invest in and learning market trends to make the best investment choices. And to be properly diversified, you’ll need to start with a big capital; otherwise, you’ll be limited in the kind of stocks you can add to your portfolio.

Bottom line: if you want the protection of life insurance, go for a VUL. If you want to participate in the growth of the Philippine economy but don’t have the know-how to go into stocks, choose a mutual fund or a UITF.

If you have the time to learn, money to invest, and aggressiveness to match, stocks may be for you.

There are a lot of options for you if you want to start moving your money out of a savings account and into a product that can work harder for you. If you are a new investor, I recommend you invest in a pooled fund first as you learn how the stock market works and develop your competency in investing. Once you’re confident that you’ve learned enough, then you can invest in the stock market.

Whatever undertaking you choose, it must have a good foundation—this is true for investments as well. Develop your base of good money management, savvy saving, and common sense, and this solid foundation will bring you real prosperity.

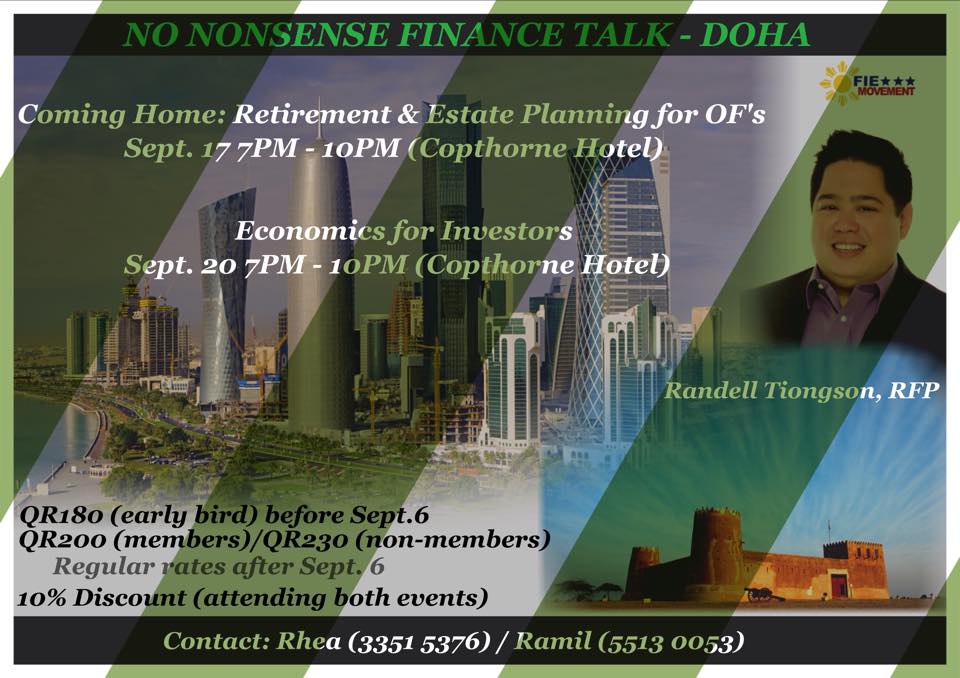

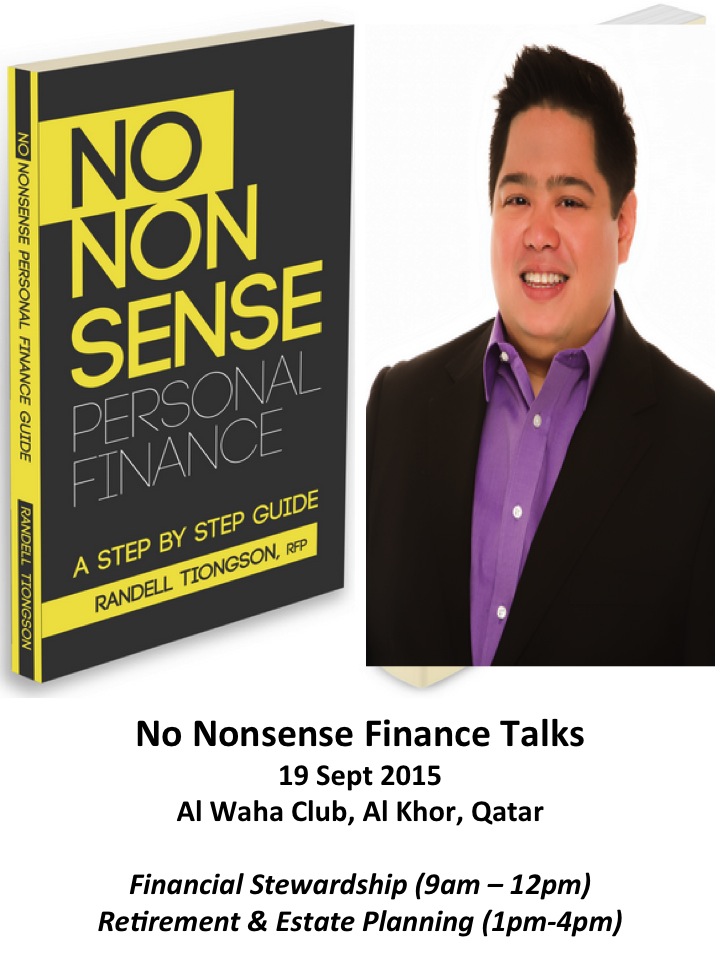

Finance events for the OFWs in Qatar

By Randell Tiongson on August 28th, 2015

I will be back for my annual series of special finance programs for the OFWs based in Qatar! This year I will running programs in 2 locations — Doha and Al Khor. The programs are organized by the Overseas Filipino Investors and Entrepreneurship Movement (OFIE-M).

Doha

a) Retirement and Estate Planning — know how to properly prepare for your retirement by learning the techniques and strategies of proper retirement preparation. The program will allow you to prepare your own comprehensive retirement program. The second-half of the program will delve into the rudiments of properly preparing for your estate in the Philippine situation. Taxes, family issues and many other problem arises when one do not prepare an estate properly.

To register, click HERE

Al Khor

A) Financial stewardship – what is the true value and purpose of money? Why is money really important? We can honor or dishonor our creator with the way we handle our money. This FREE event is for everyone who have a lot of questions on the true purpose of wealth.

b) Retirement and Estate Planning – the same program in Doha will be available for the OFWs in Al Khor

To register, click HERE

When the stock market takes a dive, what should you do? Part 2

By Randell Tiongson on August 26th, 2015

My post yesterday was viewed so much which means many people are really concerned with what’s happening in the stock market so I might as well write a follow-up.

Let me remind that the stock market volatility is the nature of that kind of investing which is why investing in equities is for the risk takers. Remember, high potential returns are high risks in nature. The external factors have taken over the sentiments of people. Fear was the predominant emotion running in the past few days but yesterday’s trading saw a buying action – it seems that there will be very aggressive investors who wants to do bargain hunting. The trading halt due to the technical glitches did not dampen the buying spree, which resulted to a higher index by the end of the day. Will the low stock prices continue to attract the buying momentum? The US equities saw some up in the earlier time of their trading day yesterday but ended down by later part of the day.

When the market dives, should you dive with it? Should you hold on to your stocks or equity funds and wait for it to recover or should you cut loss already and wait for an opportune time to come in again? Well, it really depends on your objective, conviction and strategy. Why are you investing in equities in the first place? Is it to finance a long-term goal like retirement or education of your kids or is it so you can finance your vacation next summer? Knowing why you are investing and when you will need your money will allow you to develop your investment strategy and philosophy. If you are investing because you want a comfortable retirement in 15 years, why worry with what’s happening today? The stock market has proven that when you invest long enough, you will experience good capital growth with your investment.

What should you do now? Well, if you are aggressive enough you can start buying selectively but it might not be a good idea to empty all your savings and buy now as you might end up catching a falling knife. If you are investing through equity funds like mutual funds, UITF or VUL, you might want to consider adding in tranches and not all at the same time. You may also consider waiting until you are certain that the dust has settled just to be sure. Your action will now be according to you and your convictions. Just make sure to always keep in mind your objectives, time frame and risk tolerance. Also, invest money that you are not planning on using in the next 2-3 years.

Just like yesterday, I asked more of my expert friends as to their thoughts and advise regarding the current stock market condition:

Markets tend to have knee jerk reactions to global events, and selloffs are often self-feeding which can result in steep drops. Longer-term, however, historically it’s the fundamentals which have dictated where markets have eventually gone. So if your view is long-term, it may be good to remember that Philippine fundamentals are solid. – Riza Mantaring, CEO of Sun Life of Canada Philippines

As we all know the market correction is driven by the fear that the Chinese economy will no longer be the accelerator behind the global economy. This resulted in an almost 40% reduction of the stock market in Shanghai, which as many Chinese individuals invest their savings, is expected to also impact the domestic demand in China. The reaction however seems to be extreme and mainly caused by panic, as medium and long-term prospects for the region are still positive. My advise is to not try to catch a falling knife, but prepare and be ready to increase holdings at discounted prices when the market becomes a bit more stable in the coming days. – Rien Hermans, CEO of AXA Philippines

Stock markets would always be volatile, it is because of this volatility that above average earnings is possible, embrace volatility! – Alijefty Gonzales, investment advocate & VP of Insular Life

The huge drop in the market over the recent days is an opportunity for long term investors to accumulate. It does not mean that you will not lose money in the short term but it does mean you will earn over the long term. Remember time in the market is more crucial than timing the market. Their emotions when investing especially at times like these sway a lot of people. Stay strong! Keep calm! Live well! This is not the end of days; in fact it is bargain-hunting days! Moderate your investment purchases in tranches over 3-6 months or even 1 year. – Jess Uy, Global investing advocate.

Live a life of wisdom and faith, not of fear!

Here is a easy to understand infographic from Time that will help you understand the factors that are affecting the stock market today.