The Types of Non-Life Insurance and Which One You Need

By Randell Tiongson on February 27th, 2016

‘Gastos nanaman…’

‘Hindi pasok sa budget eh.’

‘Kailangan ba talaga yan?’

These are common statements uttered when it comes to insurance policies. Insurance are to, you guessed it, ‘insure’ the policy owner and his beneficiaries – to protect (through monetary compensation) in the event of an unfortunate event such as an accident. The words ‘insure’ and ‘protect’ are powerful; however, many Filipinos do not understand the value of insurance policies, more especially non-life insurance, also known as property and casualty insurance.

Characterized by close family ties, Filipinos value familial relationship, and this can be seen by parents putting their children through school and children funding their parents’ retirement (this is another story). In a 2013 survey by Sun Life entitled, Study of Lifestyles, Attitudes and Relationships (SOLAR) – Financial Literacy Advocacy Report (FLARe), a third of Filipino respondents consider life insurance as priority purchase for the next two years. Life insurance provides protection to the policy holder’s beneficiaries in the event of a major and fatal accident. Filipinos, who are culturally-known to be family-oriented, are starting to understand the value of life insurance.

How about non-life insurance? What exactly is it? And when do you need one?

Non-life insurance spans different categories, and which one you need is dependent on your personal situation and preferences. You can have more than one type of non-life insurance. The important thing to note is non-life insurance is valuable, and you should consider getting one if your situation calls for it.

Below are the different types of non-life insurance and a checklist to determine if you need the following:

Car Insurance

As the name itself says, car insurance insures your car (and the riders) in the event of accidents resulting from both natural (e.g. typhoons, floods, etc.) and man-made (e.g. theft, exterior and interior damages) occurrences. The average annual cost of car insurance for a Toyota Vios (1.3 Base M/T) is about Php 18,000. You can do a lot with Php 18,000, so why put it in car insurance? The answer is to protect yourself from financial disaster. An annual premium of Php 18,000 is a small price to pay in the event of a major accident where repairs can cost well above a hundred thousand pesos or when your vehicle is totaled and needs replacement. Now, the Php 18,000 doesn’t seem like such a burden when put beside a repair tab of Php 100,000.

Comprehensive car insurance includes protection against accidents and theft and provides roadside and sometime medical assistance and coverage as well.

When should I get one?

If your car is your primary means of transportation (e.g. you use it regularly)

If you drive on roads that are accident-prone (e.g. susceptible to traffic, theft, natural disasters, etc.)

If you have a vehicle. It’s the law (for Compulsory third party liability (CTPL) insurance).

Home Insurance

Home insurance functions in the same way as car insurance does but for your home instead. Owning a home is part of the Filipino dream, and real estate is the preferable investment (over paper assets) in this country. With the importance of real property in this country, it should be a given to protect one’s home at all costs; however, not many consider getting home insurance, especially with the annual premiums that reach the high five-digit mark. You may be thinking that your house is sturdy, made of concrete, and has a stable foundation, so why bother with home insurance? As mentioned above, the annual premiums are a small price to pay in the event that you make a claim. An annual premium in the five-digit range will give you a coverage valued in the millions.

Home insurance provides coverage from natural disasters, robberies, and water damages and may offer additional benefits such as a relocation allowance, legal assistance, and medical (ICU) assistance.

[ File # csp0027902, License # 1743072 ] Licensed through http://www.canstockphoto.com in accordance with the End User License Agreement (http://www.canstockphoto.com/legal.php) (c) Can Stock Photo Inc. / webkingWhen should I get one?

If you live in an area prone to natural disasters such as floods, typhoons, earthquakes, fires, etc.

If your home (e.g. secondhand) has a history of being neglected and is prone to water leaks and bursts, pipe damage, etc.

If you live in an area prone to malicious events such as thefts

Fire Insurance

Fire and home insurance policies are sometimes used interchangeably since the coverage they provide are almost the same. The main thing to note is that whether you get home or fire insurance, always read your policy, page to page. Ensure that all the points you discussed and agreed with your insurance agent are all stated in the document. This way, it doesn’t matter whether you opted for home or fire insurance. If the coverage you want to make a claim for is stated in your insurance policy, then there’s no need to worry.

When should I get one?

If you live in an area prone to fires and other natural disasters such as floods, typhoons, and earthquakes

If your home (e.g. secondhand) has a history of being neglected and is prone bursting of water systems

If you live in an area prone to riots and strikes

Travel Insurance

Many tend to forego of travel insurance because of the additional expense. Php 800 for insurance to cover your single-entry trip to a country in Asia may not seem much, and besides, there hasn’t been an instance wherein you thought – ‘I wish I had travel insurance’. However, the insurance premium is a small price to pay in the event of an accident, such as losing your luggage. If you plan to travel far away (e.g. from Southeast Asia to Europe) and expect to buy a lot of new belongings, maybe you should consider travel insurance for this once-in-a-lifetime trip.

When should I get one?

If you possess or expect to bring home valuable items

If your carrier has a reputation of providing sub-par services (e.g. flight delays, trip cancellations, etc)

If the carrier has received negative feedback from customers (e.g. lost or opened baggage, flight delays and cancellations, etc.)

Deciding on a Non-Life Insurance Policy

Hopefully, the tips above have shed light on the need-to-know regarding non-life insurance. There are different types, and the need for each one is dependent on different factors. If you’ve decided on applying for one, be it car insurance or home insurance, financial comparison platforms, such as MoneyMax.ph, compare non-life insurance policies from different providers to give you the most bang for your buck.

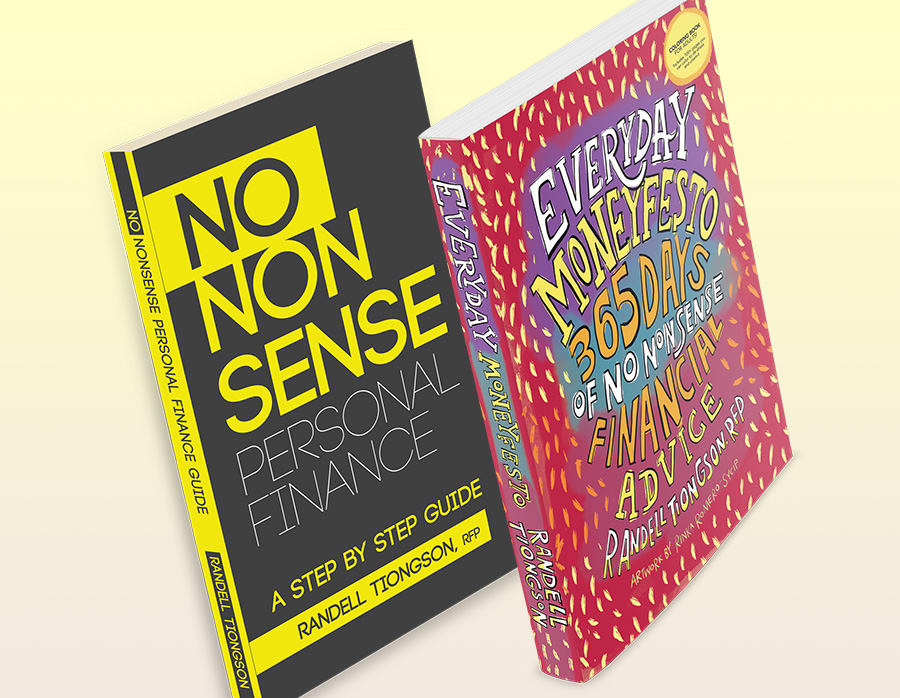

Awesome book bundle promo!

By Randell Tiongson on February 25th, 2016

Here’s your chance to get 2 of my books at an awesome bundle promo!

No Nonsense Personal Finance: A Step by Step Guide— This book will take you to a step by step and instructional process on how to achieve financial peace the no nonsense way. On its 5th printing in just 2 years, this book has sold over 15,000 copies already. I have received so much feedback that No Nonsense Personal Finance has been a big help to so many and their testimonials are encouraging. This book outlines the 5 steps for you to help you achieve your financial goals.

Everyday Moneyfesto: 365 Days of No Nonsense Financial Advise — My latest book released last December 2015. This book is a book of financial wisdom given in daily short but powerful quotes that can help you bring you closer to financial freedom day by day. In 2 months, this book has sold 2,000 copies already despite not being available in bookstores yet.

For a very limited time only, you can grab a chance to own both books with my latest promo. The regular price of both books is at P 1,100.00 but if you avail this bundle, the promo price is only P800.00 — a savings of P300.00 for both books!

But you need to do this fast as my promo ends on March 15, 2016.

To order, follow these easy steps:

Deposit payment to BPI 0249-1113-09 under John Randell Tiongson

Send a photo of the deposit slip to michael@randelltiongson.com along with your complete address and contact number.

Free delivery for Metro Manila orders, for provincial orders add P100.00.

Wait for your book/s in a couple of days.

Personal Finance for Millennials: Maximizing Today for a Better Tomorrow

By Randell Tiongson on February 24th, 2016

They’re the ones born between 1982 and 2002. The world seems to have a love-hate relationship with this group, and numerous articles have sprouted up titling this group as entitled, lazy, and narcissistic. They can’t seem to stay at one job for too long and expect too much, too soon. Who else are they?

The millennials.

However, if you look at the other end of the spectrum, you’d be surprised at what you’d find. When it comes to personal finance, millennials start saving for retirement at an early age than any other generation. According to the Investment Company Institute, the average age millennial households start saving for retirement is 23 versus the 35 of baby boomers (1946–1964). Even further, in the 2015 Deloitte Millennial survey, 6 out of 10 millennials in emerging markets including the Philippines are ambitious in attaining leadership positions.

Saving for retirement in their 20s? Striving to climb the corporate ladder? These habits may have been born out of a need or through experience – whether it’s seeing their parents lose savings or their homes during the 1997 Asian Financial Crisis or the 2008 Financial Crisis (for others experiencing this tumultuous period personally).

So how has the money game changed for millennials? And how can they start today for a better tomorrow? Here is what you need to know when it comes to personal finance for millennials:

Valuing experience over material goods

In an Eventbrite survey targeting millennials, over 75% or 3 out of 4 people preferred to spend money on experiences rather than material goods. Experiences can range from attending concerts and other events to traveling domestically or internationally.

How does this relate to personal finance? It takes discipline to save up for a ‘travel fund’, and when it comes to money management, it all boils down to habit. Are you indebted with loans? It’s important to build the habit and pay your balance monthly. Did you buy a ‘piso’ fare to Korea or Japan and now need to save up for pocket money? You need to build the habit of saving a portion of your income every month for your future expenses. If you want to experience life instead of being confined in your cubicle, you will need money, and you’ll need to learn how to control, budget, and save.

What is the takeaway? Experiences come at a price since nothing in this world is free. It’s important to build the habit of budgeting and saving so you can experience what life has to offer.

Taking advantage of restlessness

Millennials have a reputation for being job hoppers. Using data from the Bureau of Labor Statistics, the average worker stays at each job for about 4.4 years. For millennials, it’s half that number. Furthermore, 91% of millennials expect to stay less than three years at a job. Whether it’s because of burnout, employer disloyalty, or a career change, many millennials are looking at the next opportunity. They’re restless for new experiences and opportunities. Again, how does this relate to personal finance?

If you can’t sit still for too long, maximize this, whether it’s negotiating for a higher salary when switching jobs or staying with your current employee while multiplying your income streams. For the former, moving jobs can garner you a salary increase between 10% to 20% (or more) while an average raise is at 3% according to the Consumer Price Index of the US Bureau of Labor Statistics. As for the latter, multiplying your income streams will require more effort but result in more disposable income.

What is the takeaway? If you’re the type of person who’s always restless, always itching to do something or looking for the ‘next’ thing, busy yourself in such a way that will benefit your personal finance. Whether it’s moving jobs after two or three years because of no internal growth or looking for ways to earn more, there are multiple ways to keep busy and grow your finances.

Maximizing the digital space

Life, in general, has become more convenient in this digital age. Flight tickets can be booked online. Shopping can be done without going to a brick-and-mortar store. Your money matters are no exception. Transferring money can be done with online banking. Applying for a Philippine investment account can be done by OFWs from their country of employment. Even when it comes to researching for the best credit card, loans, or car insurance, you can do your research and consultation without having to go through a bank or insurance provider. Comparison portals present the information you need when it comes to financial products.

What is the takeaway? Use the worldwide web to your advantage and to help you when it comes to personal finance and money management. Comparison portals save you the time and money when it comes to searching for the credit card or loan with the lowest interest rate. There are apps available for both Android and iOS which help you track your expenses, manage your debt, and report your investments. I actually wrote an article on this entitled, Online Hacks and Apps for Your Personal Finances. If you want to learn more about personal finance and how to handle and grow your money, there are multiple online resources and blogs which you can read for free. Maximize the digital space for a financially and holistically better life.

Personal finance for millennials – it can be a tricky topic. Each generation has similarities and differences, money habits included. Hopefully, the three points above have shed light on how millennials can maximize today for a better tomorrow and brighter financial future.

Let no one despise you for your youth, but set the believers an example in speech, in conduct, in love, in faith, in purity. – 1 Timothy 4:12, ESV

Want to learn how to manage your finances better?

Register now and get a free copy of my e-book. Start your financial planning journey today!

![[ File # csp0027902, License # 1743072 ] Licensed through http://www.canstockphoto.com in accordance with the End User License Agreement (http://www.canstockphoto.com/legal.php) (c) Can Stock Photo Inc. / webking](https://www.randelltiongson.com/wp-content/uploads/2016/02/home-insurance.jpg)