7 reasons why the Philippine economic growth is not a bubble in disguise

By Randell Tiongson on November 26th, 2013

A Forbes columnist recently wrote an article that stirred up a hornets’ nest. The post called out the Philippine economic miracle as a bubble in disguise. While the author has some valid points we should not ignore, many of us do not agree. The Philippine economy is the fastest growing economy in Southeast Asia and one of the fastest in the world!

So, is the Philippine economic growth really a bubble in disguise? Our answer is a flat no!

I recently had a conversation with my colleague, economist Dr. Alvin P. Ang who is also the President of the Philippine Economic Society. We both felt that the analysis is rather thin and is not very accurate. Truth to be told, his analysis seems to be delinked from our reality.

Here are 7 good reasons why the Philippine economic growth is not a bubble in disguise:

1. The Philippines has enough guarantees (learning even prior to 1998 Asian Crisis) on RE (real estate) bubbles. Banks are not allowed to lend beyond 25% of their portfolios to real estate. The RE market is clearly differentiated into segments and the large bulk affordable to people is not necessarily facing a bubble.

2. Debt to GDP ratio is now low. Majority of the current debts are long term in nature.

3. Stock market already corrected more or less mirroring GDP growth valuation.

4. Our consumer spending has been growing for years – this is financed largely by OFW remittances.

5. OFW remittances are not coming mostly from the US. Our workers are spread all over the world – this is the reason why the 2009 crisis barely affected remittance growth. Besides, BPOs also has a significant contributing factor and also spreading beyond call centers to higher value added outsourced work. The current account position or the short-term foreign exchange payables are in surplus – a far cry from our situation in the 80s and 90s. Are reserves are now in record high!

6. Car sales are increasing not only due to low interest rates, but also because car prices have become lower relative to total income.

7. We are not having a credit bubble when loans to GDP is only 51% one of the lowest in Asia. Non-Performing Loans (NPL) as % of total loans is at all time low of only 2.7% – suggesting the better quality of loans.

Nonetheless, sustaining the current growth path and avoiding any bubble requires that the country take advantage of the low interest rate regime by shifting to productive activities. The concern is the required structural adjustment to match the need for employment growth.

Furthermore, the rebuilding requirements of the devastated areas will push public spending higher cushioning any potential RE bubbles. There is nothing wrong with government spending for infrastructure, as this is what is needed to sustain the growth. With the rebuilding process, government will not be affected by external interest rate fluctuations as multilaterals like Asian Development Bank and World Bank will lend at concessional rates. This will most likely be followed by ‘bilaterals’.

Finally, it is time for local investors and entrepreneurs to believe in this country and not be swayed by external opinions. After all, we live here. It is only us who can disprove opinions made from outside without coming here and studying the country in detail.

The Department of Finance issued a statement in reaction to the “bubble” article featured in Forbes:

———————————

DOF ECONOMIC BULLETIN

25 November 2013

The Philippine economy is not experiencing a bubble, contrary to a Forbes article on 21 November 2013.

First, the current account in the BOP is in surplus, by 4.2% of GDP in the first half of the year. This implies that the economy has more savings than  investment and is even a net lender to the rest of the world. Compared with the 1997-98 Asian crisis, all ASEAN countries except Singapore then had current account deficits. (Hong Kong and China were also in surplus.)

investment and is even a net lender to the rest of the world. Compared with the 1997-98 Asian crisis, all ASEAN countries except Singapore then had current account deficits. (Hong Kong and China were also in surplus.)

As a result of the robust current account, the country’s international reserves are piling up — rising from US$81.7 billion last year to US$83.4 billion in October 2013, equivalent to a year of imports of goods and services, one of Asia’s highest. Compared with 1997-98, ASEAN reserves were equivalent to 1-2 months of imports and were declining at a fast pace until the IMF stepped in to assist these economies.

Second, the inflation rate is manageable at 2.9% in October 2013 — still within the 3-5% Bangko Sentral target. In 1997, ASEAN economies had an average inflation rate of 6.1% and this rose to 15.1% the next year.

Third, the exchange rate continues to be stable, moving just slightly outside the P41-43/US$ range. The 4.2% peso YOY depreciation in October 2013 is far from the 13.1% and 53.8% ASEAN depreciation in 1997-98.

Fourth, the budget deficit is estimated at 1.2% of GDP as of September 2013 — lower than the targeted 2% of GDP. The 35.8% infrastructure spending in the first half of 2013 is due more to realignment of spending priorities than excessive spending.

The strong BOP and fiscal accounts and low inflation do not indicate that a bubble exists.

Colombo mentions some indicators showing a bubble, as follows:

1. Soaring capital inflows – The capital inflows he is referring to are OFW remittances and BPO revenues which have proven to rise even under the worst economic conditions in the West. Personal remittances of OFWs rose 9.7% last year and 6.6% as of September this year even if Europe was in crisis and US was not growing.

2. External debt spike – External debt of the Philippines has been declining from US$60.4 billion in 2011 to US$60.3 billion in 2012 and US$58.1 billion as of June 2013. As % of GDP, this are equivalent to 27.0%, 24.1% and 21.6%, respectively.

3. FDI has boomed during the last 10 years – We would be happy if this were true. FDI has averaged less than 0.9% of GDP during the past 5 years.

4. PSE has tripled since 2009 – The sharp PSE rise (32% average during the last 5 years) just mirrored the sharp rise in corporations’ net income (28.4% rise).

5. Inflating property bubble – The rise in prices and rentals of residential properties in Manila CBD are not a sign of a bubble but are in fact due to rising demand and low supply. Eventually, prices and rentals will go down as new supply comes onstream. As of 2013 Q2, vacancy rate is 9.8% and 4.3% for residential and office space, respectively. When vacancy rates drop below 10%, prices and rentals rise. It is necessary to keep on building to reduce impact on prices.

———————————

We must continue to pray with and for our nation: “Blessed is the nation whose God is the LORD, the people he chose for his inheritance.” – Psalm 33:12, NIV

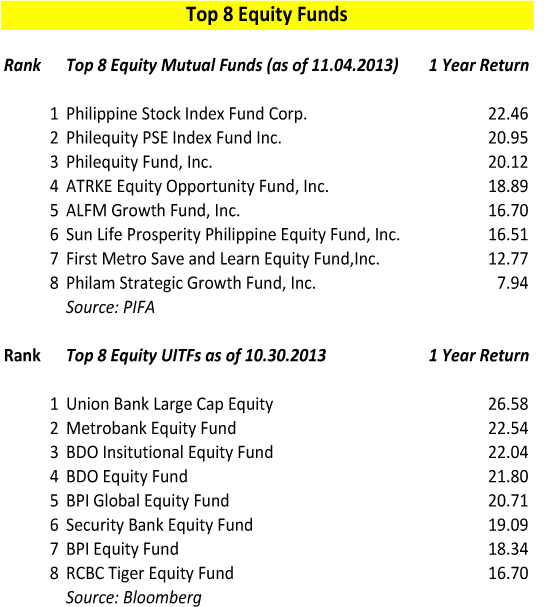

Top 8 Equity Fund Performances

By Randell Tiongson on November 5th, 2013

The year is almost over and this has been a whirlwind of a year for the Philippine Stock Markets. The start of the year saw a tremendous surge of the market pushing the Philippine Stock Index beyond the 7000 mark. Towards the middle of the year, massive correction and decline was seen as foreign funds took profits but our market seems to be more resilient than ever. Some recovery was seen pushing the market up again and refusing to enter a bearish market. Our market has yet to go back to the 7000 mark but many analysts are confident we will be back to those levels sooner than later, perhaps early next year?

For those who invested in equity pooled funds like mutual funds or Unit Investment Trust Funds (UITF), it is good to know that there continues to be good returns although not as substantial as 2012. I have collated the 1 year returns of the top 8 equity funds, both mutual funds and UITFs. On the mutual funds side, the 2 index funds rose to be the top performers for the 1 year period lead by the Philippine Stock Index Fund and the Philequity PSE Index Fund. Customarily, managed funds outperforms the index, but that’s not the case for this 1 year period. On the other hand, some UITFs performed better than the index funds and 5 of those UITFs registered above 20% returns for 1 year led by Union Bank, Metro Bank and BDO and BPI. The UITF equity funds seems to be performing better than their mutual fund counterparts for the 1 year period.

Let me repost what I earlier said in an earlier post: “I need to caution readers, however, that returns are not the sole factor if selecting a fund. Aside from fees, it will be good to check on how volatile the funds are, experience of the fund manager and size of fund. Bigger funds are usually less volatile but may not have the best performance. Further, equity funds that are more diversified and having more variety in the fund is generally less risky.”

Mutual Funds are available through Mutual Funds Companies and are regulated by the SEC. UITFs are available through banks and are regulated by the BSP.

Where should you be investing your money?

By Randell Tiongson on October 31st, 2013

Q: I have been a reader of your column and blogs and I have learned much from them. I am now debt free and have some emergency funds and savings and I am now ready to invest. Where should I put my money? – Name withheld upon request, asked via e-mail

A: Congratulations for being disciplined enough to be debt free, establish your emergency funds and consider investing—you are on your way to achieving financial peace!

A: Congratulations for being disciplined enough to be debt free, establish your emergency funds and consider investing—you are on your way to achieving financial peace!

I am sorry that I can’t give you a specific answer as to where you can invest your hard-earned money as I will need to further understand your situation before I can make any recommendation.

I can, however, give you some broad guidelines, which I hope can help you arrive at a more informed decision.

You mentioned emergency funds and savings for investing, so I will try to give you my thoughts on both.

As to emergency fund, I do not recommend that you invest that, as the purpose of this money is funding against life’s emergencies.

Whenever you invest money, there is always the risk of some capital loss and there will be some form of liquidity risk involved, as you may not be able to immediately convert the investment into cash.

It is best to keep emergency funds in cash or near-cash instruments such as time deposits and treasury bills. If you are still keen on investing your emergency fund, you may opt to put some of it in very low-risk investment instruments like UITFs or mutual funds invested in the money market or bonds. Obviously, you can’t expect much return even for those funds, but I suppose it’s better than what you can get from savings and time deposits.

I recommend that you should only invest a maximum of 50 percent of your emergency funds in the instruments I mentioned and the rest should be in cash for easy access.

As to your savings on top of your emergency fund, you should consider a few things before letting go of your money.

In my book, the No Nonsense Personal Finance: A Step by Step Guide, I outlined some basic guidelines:

Know you investment objective: Before you do anything with your hard-earned money, I would recommend that you first consider what your investment objective is.

I often tell people that our objectives will determine nearly every action we make with regards to finance. It is crucial that you first determine the reason for the investment.

What is the investment intended for? What do you wish to achieve in making such an investment? Is it for retirement, future education needs of your children, purchase of an asset, or a general fund?

Knowing what your objectives are will help you choose the appropriate investment for you.

To simplify objectives, categorize the general purposes of your investments according to the results in capital growth, income generation, or both.

Certain investments will yield according to your desired purpose.

For instance, people buy real estate properties because of capital appreciation while some people buy them for income purposes.

Know your risk tolerance—Risk and return are two correlating factors that you must always keep in mind when investing.

Some people focus too much on returns and forget about risks, while others just look at risks at the expense of returns.

Here’s a very basic principle in investing—returns will always be a function of the risks you are willing to take.

The risk-return relationship is simple but fundamental. The higher the potential yields are, the higher the risks will be; the lower the risks are, the lower the yields will be.

No amount of financial engineering can change the fundamental fact of the risk and return relationship.

Determine if you are a conservative, moderate or aggressive investor. If you are a conservative investor, it is wise for you to stay away from risky investments like stocks, lest you will experience a lot of sleepless nights when markets go south.

Know your time frame—When will you need the bulk of your investments? Are you investing your money just to park it while waiting for big-ticket items such as tuition or the proper investment? Or are you investing with a long-term goal of 10 years in mind?

There are short term, medium term, and long-term objectives, and there are corresponding short, medium, and long-term instruments for such.

It is unwise to use short-term instruments such as time deposits or Treasury bills (T-Bills) for long term investments like retirement, education, and anything that has more than a three-year life span, as you will lose on inflation.

On the other hand, you should not use medium or long-term instruments such as pooled funds (Unit Investment Trust Funds or mutual funds), equities, or variable universal life insurance for short-term objectives where you will need the funds in one year or less; you run the risk of capital loss.

Emergency funds are considered short-term objectives and must only be invested in short-term and very liquid instruments.

Take time to learn more about proper investing by reading books, articles and blogs, attending seminars and go ask as many people as you can.

Investing is not rocket science and a little effort can really help you make prudent decisions on making your money grow.