Invest or pay your debt first?

By Randell Tiongson on June 27th, 2016

Question: Hi Sir Randell! I’m sorry to take up a few minutes of your time, but I’d like to ask you a question since based from research, you are one of the best personal finance experts in the country, and my concern is very much related to your expertise. My question is: Should I pay my debt first or should I invest, and then use the returns on the investments to pay the debt? I have friends who have been telling me to invest “today rather than tomorrow” but is that smart considering I have debts?—Lia via Facebook

Answer: Hi Lia! I’m always happy to help! My dream is for every Filipino to become financially free, and that starts with education—teaching the basics of personal finance.

However, education is only the first step. Execution is what is important.

The advice I give here will be useless if there’s no follow through, so I deeply suggest that after you read the column, you practice what you read.

Moving on to your question, so should you pay your debts first before you invest?There are numerous aspects to consider, but one of the more significant factors is the interest rate.

Interest rate and ROI

What is the interest rate offered by your credit card company? What is your possible return on investment (ROI)?

If the interest rate on your credit card debt is 3.5% monthly, or 42% annually, and your ROI by buying a “hot stock pick” is 100%, the answer seems like a no-brainer. Invest first and use the 100% ROI to pay the debt.

However, you have to remember the interest on credit cards is guaranteed, while returns on investments are not. You can gain 100%, but you can lose your money as well.

You’ll definitely be accruing interest payments by not paying your full credit card balance. In this case, it would be advisable to pay your debt first and invest later.

Can’t you do both? Invest and pay debt?

Yes, you can if:

You have a surplus of money coming in.

If your bonus or 13th month pay is only a few weeks away, you can use the money to pay both your credit card debt and open an investment account. If you have a credit card debt of P10,000 and are expected to receive your 13th month pay of P20,000, you can use 50% to fully pay your debt and the other 50% to open an investment account.

Your debt amount is small.

If your debt is P10,000 and you are earning much more than that, you have the room to pay your debt and invest at the same time (provided you already have an emergency fund).

Lia, I hope the guidelines here have given you more clarity when it comes to making a decision.

So should a person pay his or her debts first and then invest later? Or he or she can do both?

As you can see from the points above, it really varies and depends on a person’s situation and circumstance. Just remember that if you decide to pay your debts, invest, or balance doing both, you’re taking yourself one step closer to financial freedom.

As always wisdom is needed.

Should I prioritize insurance or investments?

By Randell Tiongson on June 14th, 2016

Should I prioritize insurance or investments? Can’t I do both at the same time?

Those are questions I get asked a lot, and I understand why a few people may get confused. Whether you scour the web for personal finance resources or read books on how to handle and manage your money, there are different answers to the same questions. Other resources suggest doing both (insurance and investments) if you have a surplus of money. In my book, No Nonsense Personal Finance, insurance, which is step 4 in my 5-step ladder system, actually comes first before investments, which is step 5.

When to get insurance first?

I advocate getting insurance first over investments if you have people depending on you. Are you an OFW supporting a family back home? Are you the breadwinner of your family? If you are, then life insurance is vital for you. You are your own greatest asset, and if something unfortunate happens to you, what will happen to your dependents – your children, your spouse, your aging parents? Life insurance is there to give you and your dependents the peace of mind that if something happens to you (e.g. critical illness, disablement, etc.), that they will have the financial ability to face challenging times. Don’t take the risk and wait for something unfortunate to happen. Your monthly insurance payments are a small price to pay if you (for critical illness) or your dependents need to make a claim.

When to invest first?

As mentioned above, life insurance is for those with dependents. If your situation is the opposite (read: zero dependents), no one will benefit from your insurance policy. When you’re a fresh graduate still living in your parents’ house, how can you expect to support dependents when you cannot fully live independently? If this is the case, then you may opt not to apply for life insurance yet until you grow older and have dependents. Another option is to apply for term life insurance instead (versus permanent life insurance) which provides coverage for a certain time.

Can’t I do both?

Yes, you can do both. There are actually financial products which combine both insurance and investments. These are called VULs, or variable universal life insurance. With a VUL, you have both an insurance policy and investment account. This is perfect for those who do not trust themselves to maintain the discipline with investing. This is because if you invest outside of a VUL such as stocks or mutual funds, it’s up to you when you want to deposit more money into your investments. If you see yourself using a surplus of money to shop instead of invest, then VULs would be a better option for you. With a VUL policy, you are forced to make your monthly payments every month because you’re paying for both an insurance policy and your investments.

However, VULs are not for everyone, and it may be better to separate your investments from insurance. This is especially so if you have already built the habit to contribute to your investments and savings regularly. If you’re the type to save first before you spend, then you’re better off opening a separate investment account instead of a VUL policy. An alternative strategy that can work for you is BTID (Buy Term, Invest the Difference). You can buy a term policy which is cheaper than a VUL and invest the difference in a mutual fund ,UITF or stocks.

Buying a VUL or employing a BTID strategy will both work for you; it’s just an issue of preference.

No Nonsense Personal Finance

Insurance and investments are only 2 out of 5 aspects of my personal finance ladder system; however, all five aspects (learning to manage money, avoiding debt, saving, getting insurance, and investing) are interrelated. If you want to achieve financial freedom or become a winner when it comes to your personal finances, it’s important to learn and practice all five. You cannot invest and insure yourself if you cannot save a portion of your salary to pay the premium. In the same way, investments become futile if your debt is greater than your investments. What is important is you learn to balance the different aspects of personal finance. Before you know it, you won’t have to ask which you should prioritize first – insurance or investment – because the answer will come to you naturally.

Want to get a copy of my book No Nonsense Personal Finance: A Step by Step Guide? You can order from us directly and we will send it to your doorstep with no shipping cost! To order, simply follow the simple steps:

- Deposit P500.00 to BPI 0249-1113-09 under John Randell Tiongson

- Take a photo of the deposit slip or transfer advise as proof of payment.

- Send proof of payment along with your complete address and contact number to michael@randelltiongson.com

- Expect your book in a few days and enjoy the beginning of your quest for financial peace.

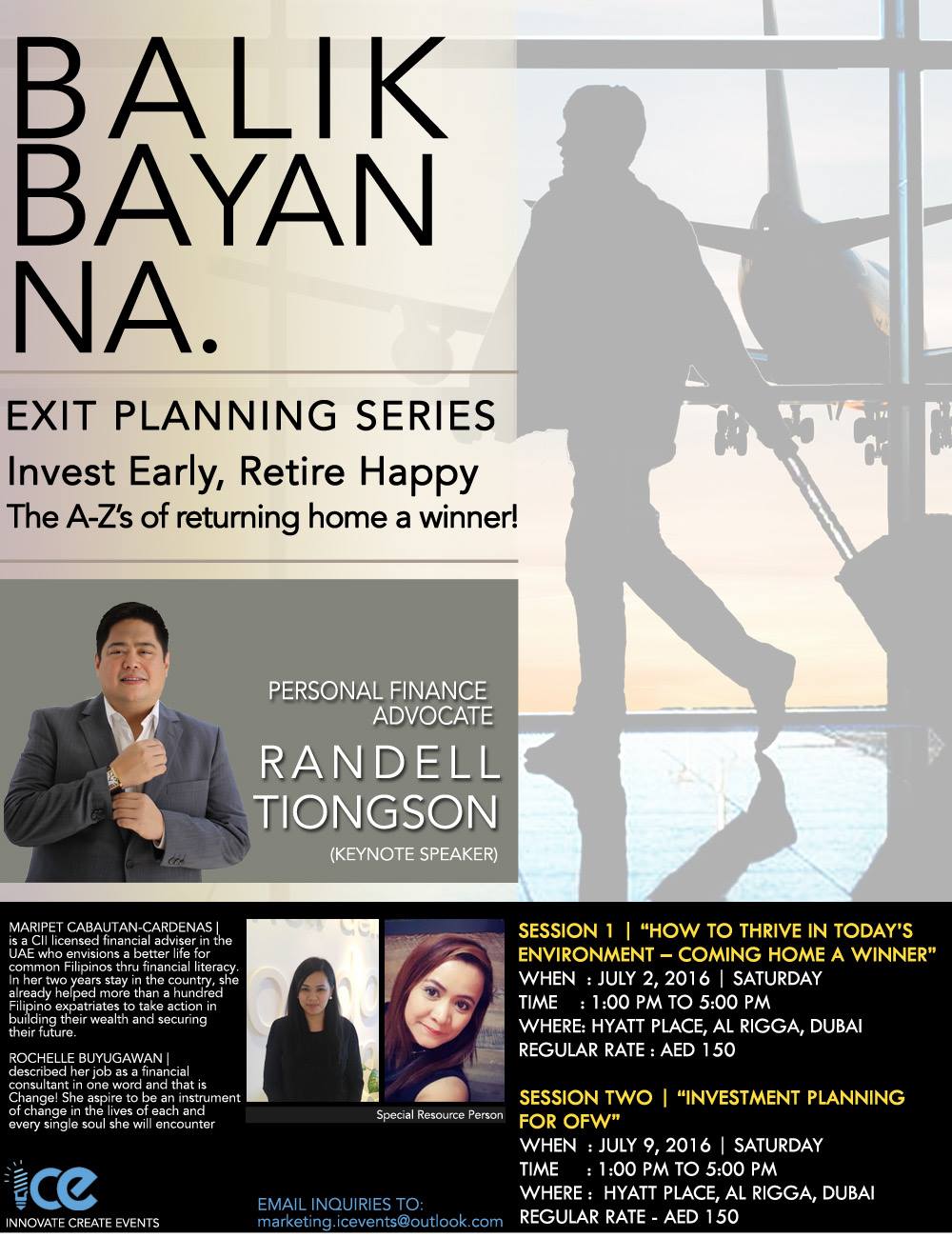

Exit Planning Series for Filipinos in Dubai

By Randell Tiongson on June 13th, 2016

Did you know that many Filipinos plan to work abroad but very few are prepared to go home eventually? Do you have the skills needed to be reintegrated back to the homeland requires? Are you prepared financially?

Join me this July 2016 for a 2-part “Exit Plan Series” which are life-changing as well as life-saving programs!

“How to Thrive in Today’s Environment” will be on July 2, 2016 and it will tackle the necessary skills and attitude to come home as a winner!

“Investment Planning for OFWs” will be on July 9, 2016 and it is all about building your wealth the right way.

Both programs will be a big help for the Filipinos in Dubai to be properly prepared with their “Exit Plan”.

To register, click HERE