Hit the books Louis!

By Randell Tiongson on March 18th, 2010

My good friend Louis is taking his post-graduate at a good university which is green (that’s why it’s good). When he told me his plans on going back to school, I told him that education is always a good idea. When he told me what he wanted to take up, I said “what?” and “why?” He is taking up a master’s degree course on Financial Engineering. Well, I said since you are young and you have the energy – go!

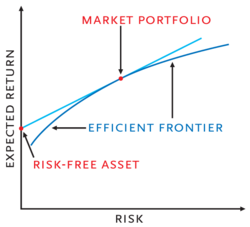

Louis and I have regular chats, over coffee or over the keyboard – in our latest chat, he was complaining about how difficult his exams are … stochastic matrices, markov chain, fractals, modern portfolio theory, CAPM, APT… etc. I told Louis a few things I know about his subjects; for instance, I said “modern portfolio theory is a theory of investment which tries to maximize return and minimize risk by carefully choosing different assets; or in other words, the concept of diversification in a mathematical formula.” Nose bleed alert!

After a few more nose bleed discussions, I told Louis… “wanna know a secret?” All those stuff doesn’t really work in today’s environment! Those investment theories will require very high IQs but will not mean squat in the real market. Theories assume that people’s behaviors are rational … the more you study the market’s history, the more you realize that rational behavior is always missing in the market. The more you try to understand what’s going on, the more you see things are fundamental… the more things go back to the basics like supply and demand. The market is a representation of people’s sentiments – and people’s sentiments are either overly optimistic or disastrously pessimistic.

So will I advise Louis to quit school? Never. Louis will need to learn all the nose bleed stuff for him to have a more intelligent view of things that are fundamental in nature. If you’re reading this Louis, go hit the books!

Is diversification rocket science?

By Randell Tiongson on February 10th, 2010

Appeared at the Business Mirror, 02.08.2010

You often hear the word “diversification” when investments are discussed. Diversification is important; in fact, it is considered one of the most effective risk-management tools, minimizing investment losses.

You often hear the word “diversification” when investments are discussed. Diversification is important; in fact, it is considered one of the most effective risk-management tools, minimizing investment losses.

What does Investopedia (a favorite online site for investment stuff) say about diversification?

“A risk-management technique that mixes a wide variety of investments within a portfolio. The rationale behind this technique contends that a portfolio of different kinds of investments will, on average, yield higher returns and pose a lower risk than any individual investment found within the portfolio.

“Diversification strives to smooth out unsystematic risk events in a portfolio so that the positive performance of some investments will neutralize the negative performance of others. Therefore, the benefits of diversification will hold only if the securities in the portfolio are not perfectly correlated.”

Diversification is often misunderstood and its execution has always been a mystery to many. To many of us, diversification is just putting your money in different banks or buying different pieces of property in different areas. However, diversification is much more than that and here are some ways to diversify:

1) By asset class—Cash or near cash (savings or checking accounts, time deposits, treasury bills or money market accounts); fixed income (government securities, corporate bonds); equities (stocks); real estate; collectibles (paintings, jewelry, etc.); enterprise (business)

2) By time frame—short term (about a year); medium term (up to about five to seven years); long term (over seven years)

3) By risk—conservative, moderate, high or speculative

4) By liquidity—highly liquid vs. nonliquid

Above are just a few ways to consider classifying your assets/investments regarding diversification. Here are some diversification tips: vary your asset classes; combine short-, medium- and long-term investments; combine highly liquid and nonliquid assets.

By practicing diversification, you are also practicing sound risk management. A properly constructed diversification strategy will minimize the risks of your investments and, at the same time, give you better yields as compared with taking an ultra-conservative position. With a good diversified portfolio, the risk of totally wiping out your wealth is highly unlikely, but at the same time, allow you to experience better growth which will be more than inflation.

But diversification also has its downside. Sometimes, a portfolio that is too diversified can also prevent you from earning properly, as the volatility of many of the players in your portfolio can cancel each other. However, having a very risk-averse position can be just as dangerous as taking a risky option, as inflation can erode the value of your wealth. The more prudent option then would be to learn diversification.

Do not be too afraid to try out diversification, it is not rocket science. Come up with a diversified program that is consistent with your investment objective, risk tolerance and time frame and you are on the road to achieving financial peace.

I really like the way the Bible talks about diversification. Yes, the Bible is a good source of investment wisdom and here’s proof: “But divide your investments among many places, for you do not know what risks might lie ahead.”—Ecclesiastes 11:2 (New Living Translation)

Since the Bible advocates diversification, I am assured that it’s a great idea.

Dreams and Deadlines, Part 2

By Randell Tiongson on December 2nd, 2009

… part 2

As financial planners, are we getting our message across? Are Pinoys any closer to financial freedom? I am elated to see more and more financial planners, more books and articles and a gazillion blogs on personal finance. I’ve seen, heard, read a lot about personal finance of late—some are great messages; while others are really rubbish, but at least the message to do something about one’s personal finance is being mentioned. Let me repeat my earlier question, are we getting our message across? From my perspective, it seems that whatever we are doing is a mere drop in the bucket, and my colleagues in this field need to realize that we are not as effective as we believe we are (apologies to bruising the egos of my colleagues).

There’s definitely nothing wrong with what we are advocating, and our message is extremely relevant. I believe that there is something wrong with the manner we convey our message. To the real world out there, we sound like condescending self-righteous bigots telling everyone they are wrong and we are right. Have you heard personal-finance speakers? They will tell you not to drink Starbucks coffee and stick to 3-in-1 or not to buy a flat TV or a new car. They will tell you that gratification is evil and will burn you. Let me use an analogy here: It’s like hearing a preacher tell you that ogling a beautiful woman will cost you eternal damnation. Yes, they are probably right, but they may not look at things from the right perspective. It’s not just about the message, it’s also about the delivery of the message.

I think it’s about time people like us realize that folks have dreams and they must enjoy these while they can. Dreams do have a deadline, as my mentor aptly phrased it. Are you going to have that dream family house when all your children are grown up and have moved out of the house? Will you buy that nice flat TV when your eyesight has become so weak? Our life has a timeline and we must act according to the set time we have. I like how the Bible puts it—“Man’s days are determined; you have decreed the number of his months and have set limits he cannot exceed” (Job 14:5, NIV). Knowing what we want in life is critical and the way we live should be reflective of our goals. It’s not all about accumulation of wealth that we should be concerned about but also the purpose for accumulating wealth.

It’s about time we really know what our dreams are and that our “dreams have deadlines”; it’s about time we know the purpose of our dreams. Oh, it’s also about time for financial planners to change the way they sing their song.

“The man who plants and the man who waters have one purpose, and each will be rewarded according to his own labor” (1 Corinthians 3:8).