5 Ways to Save for Big-Ticket Items

By Randell Tiongson on March 21st, 2016

Buying a car and owning a home – these are part of the Filipino dream; however, saving up for big-ticket expenses, such as a vehicle or a house, may seem like they will take forever. A fresh graduate earning an entry-level salary may not even be able to afford the monthly amortization for these items. A person in his thirties and forties may afford the monthly payments on a car or house loan, but paying such a large amount may be discouraging because it’s still taken out of one’s income. However, owning a car or a home is certainly possible whatever your age is. The key is building the habit – the habit to save, the habit to pay debt regularly, and the habit to stick to one’s goals.

Here are 5 easy ways to save for big-ticket items, so soon enough, owning a car or a house is your reality:

- List down your income and expenses

‘What can’t be measured can’t be improved.’ – It’s an age-old adage.

When it comes to finances, the bottom line is you have to know how much of your money is going in and going out in order to come up with realistic plan for your finances – such as buying a big-ticket item. If you don’t know how much money you’re left in a month after spending, it’ll be very difficult to come up with a payment plan that is realistic and fits your current situation.

What to do:

- Track both your income and expenses.

- Categorize your expenses (e.g. rent, utilities, entertainment, etc.).

- Set a budget according to category.

- Money going out (outflow) should never exceed money going in (inflow).

- In the next month, cut down spending on categories where you overspent.

- Sacrifice today for tomorrow

Nothing great ever comes easily, and your personal finances are no exception. If you want to live in your own home in the future or drive your own car to avoid the horrendous Metro Manila commute, you need to make a few sacrifices today for a better tomorrow.

What to do:

- Forego short-term gains for long-term ones. (e.g. don’t buy a new shirt every month and save the money instead)

- List down your long-term goals in your phone or a place where you’ll see it every day to keep your eyes on the prize.

- To control impulse spending, compare your hourly income to an item’s cost per hour, and then determine if the item’s really worth it. (e.g. if you want to buy a shirt worth Php 800, and you earn Php 200 an hour, it takes 4 hours of working to afford that)

- Save as you would pay a loan

When it comes to paying a loan or your credit card balance, the pressure is on. You’re more determined to tackle your credit card debt or loan balance with the monthly statements you receive. Worse, your balance seems to increase every month in which you don’t pay the full balance because of interest. When saving for a future expense, you’re not as pressured. You don’t have any liabilities (e.g. interest fees, defaulting, collateral) because you haven’t bought a car or a home yet. However, to build the habit of saving for big-ticket items, save for them as diligently as you would pay down a loan.

What to do:

- Know the exact amount you need for your future purchase.

- Create a savings plan (should include how much you should save every month, your timeline for saving among many others, etc.)

- Transfer a percentage of your monthly income from your payroll to your savings accounts during payday. As what Warren Buffett says, “Do not save what is left after spending, but spend what is left after saving.”

- Invest

Investing allows you to save money at a faster rate because the possible return on investment (ROI) beats the interest you earn in your savings account. However, it’s best to know that high reward equals high risk, and investments are not guaranteed. Since you stand to earn more by investing, you stand to lose a lot as well. That shouldn’t scare you away. If you’re diligent to learn and practice, you’ll become a better investor.

What to do:

- Read investment-related resources and attend seminars or conferences. This way, before you even open an investment account, you already have an idea of what to expect.

- Know your purpose or goal for investing. Are you saving for a home in the next five years or for retirement thirty years from now? Knowing you goal allows you to pick the investment most suitable to your situation and preferences.

- Don’t be a one-time investor. Once you open an investment account, put a portion of your monthly income into your investments. This way, you’ll ramp up your savings.

- Increase your revenue sources

There’s no magic trick when it comes to saving more, and there is definitely no substitute for hard work. If you want to save for a big-ticket item in less time, increase your sources of revenue, be it investing or taking a second job. By increasing your monthly income, you’ll be able to put more into savings.

What to do:

- Investing is one way to increase your revenue sources.

- Know your strengths and take up freelance gigs aligned with your strengths. People will pay you for what you are good at and for what they aren’t.

- Save ALL your income from your sidelines. Do not use the money to spend for expenses; otherwise, it beats the purpose of earning more to save more.

Living the Dream

The five steps above will bring you closer to your dream of owning a big-ticket item. Whether this is buying a car or owning a house (or another purchase), you’ll reach your financial goals as long as you build and keep the habit of saving.

Once you reach that point and buy that big-ticket item, it’s best to keep these safe. One way is to keep your discipline of saving since unexpected expenses will arise (home repairs and car maintenance fees). The need to save never really end. Another way is to protect yourself through insurance, be it car or home insurance. Insurance premiums may take a chunk of your income, but you’ll end up paying less for your insurance policy (in the event that you need to make a claim) versus than if you didn’t have insurance at all. To get the most affordable deal on non-life insurance policies, comparison portals such as MoneyMax.ph, allow you to compare different types of insurance from various providers.

You never really stop spending, but this is the importance of building the habit of saving. You never really stop needing to save even after you’ve bought that big-ticket item. Whether it’s paying down debt or saving for a big-ticket item, the key takeaway is building the habit of keeping and growing your personal finances.

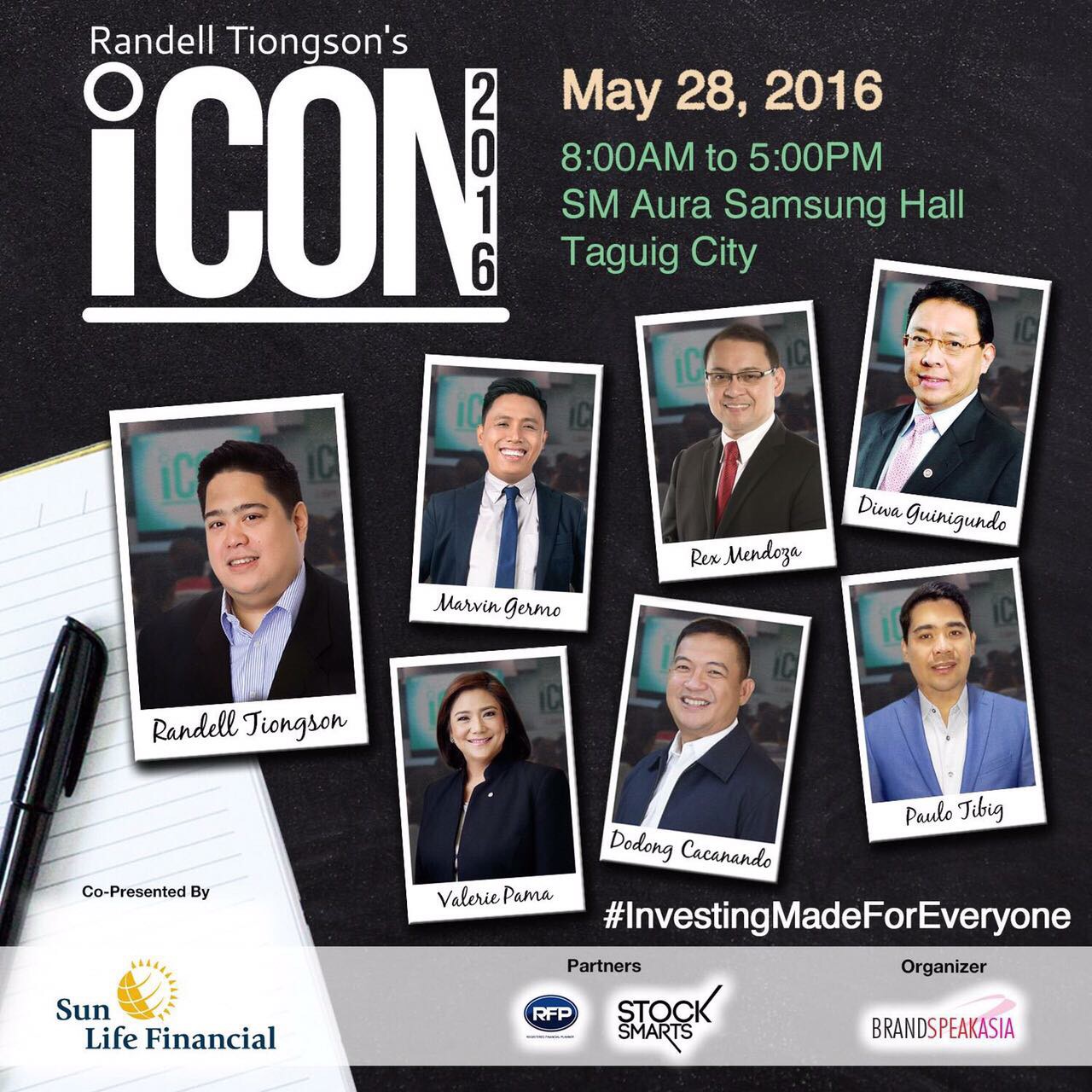

Attend the biggest finance and investment event of the year — iCon2016

Click HERE for details

Understanding (and Increasing) Your Cash Flow

By Randell Tiongson on October 21st, 2015

For today’s blog, let’s go back to basics. A lot of beginners to personal finance can feel overwhelmed because of all the options, like which investment to get or which bank to choose. But before you start on any of that, you must have a healthy cash flow first.

“The inflow of cash should always be greater than its outflow.” It sounds simple, but many people don’t have this step down yet. If you’re living paycheck to paycheck, then your inflow is exactly equal to your outflow. If you’re living paycheck to paycheck and you have debts, then your cash flow is negative.

This is where having a healthy cash flow comes in. Learning how to manage your cash will be the single greatest factor in improving your financial future, because if you don’t have extra cash, how can you start saving and investing?

In personal finance, cash flow is all about income and spending. If you’re spending more than you earn, you’ll have a negative cash flow. How can you improve this? Earn more, spend less.

Again, sounds simple, but it’s not that easy to do. To help you out, here are a few ways you can improve your cash flow:

1. Make more money. The most straightforward way to have more money is, well, to make more money. So invest in your best asset — yourself! Read books, widen your knowledge, improve your skills to expand the range of income streams you can have. For me, it was reading books that improved me; I became a better writer and teacher through reading, and I also learned a lot of things directly or indirectly related to my profession. Having more marketable skills will increase your earning power and positively influence your cash flow.

2. Invest in learning. This is a part of investing in yourself. The more you know, the more ways you can find to make money. Whether that’s by improving yourself in your current company or learning ways you can start your own business or sidelines, learning is an investment that will never go to waste.

3. Be enterprising. I’ll admit that I don’t think entrepreneurship is for everyone. However, I still think that more Filipinos can go into entrepreneurship. But it’s important that you go into it armed with knowledge — among others, you should read about the business you want to get into, observe the market, make sure your business plan is solid, and have an exit plan. It would also help to start small, such as basic buy and sell or commission selling. There are many opportunities for the beginning businessman (or woman); these 9 businesses you can start for less than P50,000 is a good jumping-off point. The number of SMEs in the country is increasing, and it’s always heartening to hear success stories. If you prepare correctly, and with God’s grace, you could be one of them. A successful business or sideline will do wonders for your cash flow.

4. Spend less money. Making more money takes time and effort. It may take months for you to get that pay raise, or even longer for your business to start raking in profits. You know what takes less effort and has immediate effects? Spending less money! I’ve said it so many times that you might feel like I’m a broken record, but it’s still true — the way to wealth is spending less than what you earn and investing the difference. If you do this for the long term, you’re sure to meet your goals.

While it may take objectively less effort to spend less than to make more, it also feels a lot more painful. We Filipinos have a culture of spending. How many times have we promised ourselves that we’d be more diligent about spending, only to go out and make unnecessary purchases?

The thing we must remember is spending on things we want, as pleasurable as it might be, is only temporary. This doesn’t mean that you should never spend money on “unnecessary” things, but you should never let it affect your financial well-being. Track your spending, identify where you can cut back, and control your spending — don’t let it control you.

Ready to get a handle on your cash flow? Having read the above, you can start by preparing a budget so you can see where your money is going and what your net cash flow is every month. Cash is the lifeblood of personal finance, so make sure yours is healthy.

Tip: Learn how to manage your finances better by reading my book No Nonsense Personal Finance: A Step by Step Guide. To order, send us an email mia.tiongson08@gmail.com

How BPO Employees Can Save and Invest

By Randell Tiongson on September 20th, 2015

The business process outsourcing industry (BPO), especially IT-BPO, is one of the fastest-growing industries in the country, expected to earn $25 billion and generate 1.3 million new jobs by 2016. Many young people now work as BPO call center agents, earning more than the usual salary for other entry-level jobs. BPO agents and OFWs are now two pillars that hold up a significant portion of the Philippine economy.

Of course, the good pay comes at a price: working irregular shifts, having long working hours, and having to deal with irate customers. But the benefits are undeniable: besides the salary, many BPO agents are entitled to bonuses when they perform exceptionally.

With all this earning power, BPO employees should start building their financial future. Here are three ways BPO employees can grow their wealth:

- Automate your savings and investments.

Automation is a saver’s best friend, because why worry about saving when it can be taken care of automatically? Savings accounts like BPI’s Direct Save-Up will automatically take out a certain amount that you set from your payroll account, and move it to a savings account where it can gain interest. Even if you have it set to something as low as P1,000 every month, that’s still P12,000 you can save every year without even trying. Check your bank for similar products.

You can take it to the next level by investing a pre-determined amount in UITFs or mutual funds on a timeline of your choice. Ask your bank what your options are, and start putting a certain percentage of your income automatically towards investment. By automating your savings or investments, you can prepare for your financial future and you won’t even feel it.

- Save or invest 50% of your performance bonuses.

One big perk of working as a BPO employee are the generous bonuses given for outstanding performance. When you receive one of these, you should be proud! But before you spend all of it by treating all your co-workers and family members to an extravagant dinner, consider putting half of it in an investment like a UITF or to build up your emergency funds if you don’t have one yet. When you combine putting away some of your bonus with regular saving and investing, you’ll reach your financial goals faster.

Then, you can still use the leftover 50% of your bonus for shopping, entertainment, or whatever you want. So you can still enjoy your money and save at the same time.

- Invest in learning.

Many Filipinos don’t like trainings and seminars, and this is a big mistake. Always take the opportunity to learn more, either in your industry or in something else. When I was a young insurance agent, I took a special certification program being offered. Many people thought it was a waste of money and time in something they saw as useless. Instead, even if it wasn’t perfect, the program made me a better insurance agent and gave me a thirst to learn more, and I was able to improve my revenue as a direct result.

So seek out programs that will give you the skills to rise in your organization; even if you spend thousands of pesos on a good program, the return on your investment will pay off in exponential ways.

Being a BPO employee is hard work, so make your hard work pay off by making good financial decisions. And remember, saving doesn’t have to be a drag; if you do it right, you can save for your future and enjoy your extra income at the same time.

Make your sacrifices count!

Join the first personal finance public chat group in Viber! Learn from experts like Edric Mendoza, Marvin Germo, Rex Mendoza, Jayson Lo, Dennis Sy, Carl Dy, Alvin Ang & more!