In 2013, I released my No Nonsense Personal Finance : A Step by Step Guide book with one clear goal: to help Filipinos become more financially responsible and free. Through years of mentoring, speaking, writing,teaching, and learning, I’ve realized that while financial strategies may evolve with time, the fundamentals remain constant. So today, I want to revisit the 5 Steps to Financial Freedom I’ve shared countless times, especially for those who are either starting their journey or finding themselves stuck somewhere along the path.

Let’s walk through the five steps again—with clarity, conviction, and a heart for lasting change. And as a bonus, I’ll share a sixth step that has made all the difference in my own journey.

Step 1: Increase Cash Flow

The first and most important step is to create positive cash flow. It’s impossible to build wealth if you’re consistently spending more than you earn.

This step requires two things: discipline and diligence. You must learn to track your income and expenses—yes, even the small ones like that daily milk tea or your streaming subscriptions. Once you see where your money goes, you gain the power to control it.

But increasing cash flow isn’t just about cutting back; it’s also about increasing income. Can you take on side gigs? Freelance work? Sell items you no longer use? Perhaps you can improve your skillset and position yourself for a raise or a better-paying job.

I always say, “If it’s important to you, you’ll find a way. If not, you’ll find an excuse.” Increase cash flow not just for survival, but so you can take the next crucial steps.

Step 2: Get Out of Debt

Debt is a thief. It steals your peace, your future, and even your relationships if left unchecked. And sadly, many Filipinos have normalized consumer debt as a way of life.

But here’s the good news: you can get out of debt. I’ve seen people dig themselves out of hundreds of thousands of pesos in loans simply by being focused and intentional.

Start by listing all your debts—credit cards, personal loans, salary loans, etc. Then, use a strategy like the debt snowball method, where you pay off the smallest debt first while making minimum payments on the rest. Once a debt is cleared, you roll over that payment amount to the next one. The psychological victories here matter more than you think.

Debt may have become your normal, but it should never be your future. My hope is that being debt-free is the new status symbol for every Filipino.

Step 3: Build an Emergency Fund

Once you’ve started freeing yourself from debt, it’s time to protect your progress with an emergency fund. Think of it as your financial shock absorber.

An emergency fund ensures that unexpected events—medical emergencies, job loss, car repairs—won’t derail your entire financial plan. Ideally, you want to save at least 3 to 6 months’ worth of your basic expenses, depending on your life situation.

And no, your emergency fund shouldn’t be in stocks or mutual funds. It should be liquid, accessible, and separate from your day-to-day account. High-interest savings accounts or money market funds are good options.

This isn’t just about being smart—it’s about being prepared. Life is unpredictable, and this fund gives you peace of mind and financial stability.

Step 4: Protect from Life’s Risks (Insurance)

One thing I often remind people of: the goal of insurance is not to make you rich; it’s to prevent you from becoming poor.

Many of us hesitate when it comes to insurance—especially life and health coverage. But what happens to your finances (and your family) if the unexpected happens and you’re uninsured? A single hospital bill can wipe out years of savings. Worse, if you’re the breadwinner, your untimely passing can leave your loved ones in a financial abyss.

You don’t need to over-insure yourself. But you must be adequately protected. Start with term life insurance if you have dependents. Make sure you have health insurance (PhilHealth + HMO + critical illness if possible).

Insurance is not an expense—it’s a hedge against financial ruin.

Step 5: Invest for the Future

After you’ve stabilized your present, it’s time to plan for the future—and this is where investing comes in.

Don’t get caught up in hype or what’s trending. Instead, start with the basics: know your goals, time horizon, and risk tolerance. Are you investing for retirement? For your child’s education? For long-term wealth?

In the Philippines, you can explore mutual funds, UITFs, stock market, PERA (Personal Equity and Retirement Account), and real estate, among others. But here’s a truth I will never get tired of saying: There’s no one-size-fits-all investment. Educate yourself before you invest. Seek professional guidance if needed.

And remember—investing is not gambling. It’s a long-term commitment to your future self.

Bonus Step 6: Start Tithing

Now, let me share something deeply personal and spiritual—something that has had a profound impact on my financial journey: tithing.

I firmly believe that everything we have is ultimately from God. Tithing isn’t about giving back a portion—it’s about honoring the Giver. Proverbs 3:9 says, “Honor the Lord with your wealth and with the firstfruits of all your produce.” (ESV)

When we tithe, we realign our hearts. We break the grip of greed and acknowledge that God is our true provider. I’ve seen it in my life and in the lives of countless others: when you put God first, He faithfully provides—not always in ways we expect, but always in ways we need.

Tithing isn’t just an act of faith—it’s also a powerful habit that shapes our character, our financial decisions, and our purpose. If you want real financial freedom, it must include surrender—because money is a heart issue, not just a math problem.

A Brotherly Reminder

Financial freedom isn’t just about numbers—it’s about mindset, discipline, and for me, faith. It’s about understanding that your financial life is a journey, not a quick fix.

My 5 (now 6!) Steps to Financial Freedom may sound simple, but they require consistent action and heart-level change. Whether you’re just starting or rebooting your journey, I want to encourage you: It’s never too late to start making wise financial decisions.

I’m still walking this journey too, and I’m glad we can do it together—one no-nonsense, God-honoring step at a time.

5 tips to get rid of your credit card debt

By Randell Tiongson on August 27th, 2017

QUESTION: Because of emergency and other unforeseen expenses, I have racked up credit card debt. I hate the feeling of having debt. It scares me that I may never be able to pay them down, and the interest rates are discouraging. I would love to get some tips from you on how I can pay down my debt. Thank you so much for your help. – Johnny via e-mail

Answer: Ah yes, when you have credit card debt, it can feel like there’s a heavy weight on your shoulders. You want to do a number of things, but you can’t because you’re always thinking about the debt you have. It feels hard to relax when you pay more on interest month per month. Eradicating credit card debt will take a heavy weight off your shoulders. If you’re up to neck in debt, here are 5 easy tips to get out of credit card debt:

Use the snowball method

The snowball method is a method used to tackle debt by attacking your credit card with the smallest balance first. Just as a snowball is rolled and piled together to create a bigger snowball, the snowball debt method lets you start with the smallest balance to give you the confidence to attack bigger balances in the future. Paying off the smallest balance will make it easier and faster for you to pay down debt. For those who are new to saving and budgeting, starting small (read: paying the smallest balances first) will ease you into the habit of paying debt. If you start big and pay off the biggest balance with the highest interest rate first, this can shock you and make you feel like you’re not making any progress and you might fall back into the trap of accumulating more debt.

Automate payments

“Out of sight, out of mind” right? If you set up your account, so that your credit card dues will be automatically debited from your bank account, you’ll treat the money as if you never had it at all. If you choose to pay your credit card balance manually, you may be tempted to pay the minimum balance only to give way to other expenses you prioritize. By automating your credit card payments, you’ll feel like you didn’t even have the money in the first place. Even better is that you’re paying the full balance each month, which avoids extra fees. Multiple banks, such as BDO, BPI and HSBC, offer this auto-payment service. Just log on to your online account to apply.

Track your expenses

A lot of people get into credit card debt because they treat it as free money. It’s easy to hand that plastic to the register, swipe it, then sign. Until the billing statement comes. Then, you find yourself searching every corner of your home for spare change to pay your balance. By tracking your expenses (pro tip: have a separate category for credit card expenses), you’ll see where your money is going, and you’ll realize just how much you’ve racked up in purchases using your credit card. Tracking your expenses avoids adding to the debt you already have. Multiple phone applications, such as Expense Manager, Mint and You Need a Budget, allow you to track your expenses in a comprehensive manner (e.g. by timeline, by category, current balance, etc.).

Transfer balances

Multiple banks provide this service of transferring and consolidating all your credit card debt into one bank. To get the most out of balance transfers, transfer all your balances to the bank that offers the lowest interest. This way you’ll be paying less in interest, which can save you a lot. Late fees for credit card dues start at around 3 percent a MONTH, so it’s best to avoid sky-high interest rates as much as possible. By transferring your balance from one account with a high-interest rate to the one with the lowest, just imagine how much you can save. It’s best to remember that there’s no such thing as free money and the interest rates on credit cards will make you wish you never had a credit card in the first place.

Use a part of your savings

Have an emergency fund, it’s one of the basics of personal finance. This e-fund must be used ONLY for emergencies, nothing less; however some rules can be broken. If your e-fund is well-padded, if you have a continuous flow of income, if you have a partner that has his or her own income and emergency fund, if you have investments, THEN you can use a portion of your emergency fund to make a lump sum payment. Remember that in a savings account, you only earn 0.25 percent in interest a year, humiliatingly less than the 3 percent a month you pay in credit card interest. Consider using a portion of your savings to pay your debt down faster and avoid incurring the 3-percent interest a month.

Road to financial freedom

It’s a different feeling when you don’t have to worry about debt. You don’t feel like you have a rope tied around your neck. You feel like you’re able to save and invest earlier and faster. Having zero debt maximizes your opportunity to live a life free of worries. That portion of your income you used to pay down debt? Use that money to go on a much-needed vacation that is not funded by debt. Even better, use the money to start investing, saving for a house down payment, or whatever financial goals you may have. The bottom-line is once you pay down all your credit card debt, you’re on the fast track to reach a life free of money worries.

“The rich rules over the poor, and the borrower is the slave of the lender.” – Proverbs 22:7, ESV

Sign up for my financial planning diagnostic system for FREE! Visit https://parachure.com/

Are you on the right path to financial freedom?

By Randell Tiongson on May 24th, 2016

What is financial freedom? It sounds like a heavy word. In reality, financial freedom is being able to afford and do what you want, when you want it. This could be having the ability to buy material things without thinking about the cost. This could be retiring early, way before you hit sixty. This could be having the power to quit your job and pursue passion projects, be it starting a business or giving back to the community. Financial freedom sounds like a dream, but if you look around, you may know of some people living the dream, living financial freedom. Do you want to reach financial freedom as well?

Here are 5 points to determine if you are on the right path to financial freedom:

1) You don’t worry about last-minute emergencies

Car broke down? Are you feeling aches and need a trip to the doctor? Other people may hold off having car repairs and medical trips because of the expenses they will incur; however, if you have an emergency fund and even health and car insurance policies, you won’t even think twice of taking your car to the shop or having a doctor’s appointment. If you find yourself panicking during emergencies because of finances, then that’s a sign that you have money problems. If you’re on the right path to financial freedom, you find yourself having the monetary means to pay for last-minute emergencies.

2) You have a positive money mindset

There are people who balk at the idea of having credit cards or loans. “Credit is evil and should be avoided at all cost” is an exaggeration but a very true statement you may hear. It’s time to change that mentality. Credit can be good for you if you use it to your advantage. This means paying your credit card balance in full or taking out loans to set up your future, such as taking out a house loan to buy an investment property. By having a positive money mindset, you’ll learn to make money work for you.

If you want to build a positive money mindset, you can start with reading online blogs, such as mine, and educate yourself on personal finance. At present, self-education is easier than ever what with the multitude of resources available. Even when it comes to applying for a credit card or a house loan, the information and resource you need can be found through comparison websites, such as MoneyMax.ph. The availability of finance-related resources makes talking about money more accessible. The more you read about personal finance, the more you realize that money isn’t as scary or evil as you may have originally thought.

3) You have a healthy savings account

Do you know someone who earns so much and yet always complains about being broke? At the same time, do you have a friend who may not earn so much and yet never complains of not having enough? Between the high and the low-earner, the latter is the one closer to financial freedom. Having a large salary becomes futile if you save 0%. What happens during retirement when you’re not earning a salary anymore? To be closer to financial freedom, start with having a healthy savings account. This means saving a portion of your salary every month. It’s even better if you have a large income; this means you’ll be able to save more. Remember, you cannot invest what you do not save.

4) You know how to say ‘no’

Whether it’s saying ‘no’ to that new pair of shoes or saying ‘no’ when your friends chide you to treat them to another round, having the ability to say ‘no’ can do wonders for your finances. If you track your expenses, you will notice that the little things add up. A cup of Php 100 coffee may not seem much, but drinking one every day of the working day adds up to Php 2,200 a month, or Php 26,400 a year. By learning to say ‘no’, you’ll be able to do your finances some good. Learning how to control your impulses and building the habit will have positive effects not only when it comes to your finances but yourself as a person.

5) You’re making money while you sleep

You may find yourself raising an eyebrow. ‘Making money while I sleep? Is that even possible?’ Yes, it is, and it can be done through investing. I mentioned earlier that employees lose their primary source of income when they reach retirement. This means they won’t be earning a salary anymore, and yet, they’ll continue to spend. If you reach retirement and you have insufficient savings, how will you cover your expenses? You can start investing.

However, don’t start investing when it’s already too late, start as soon as possible. To stay on the right path to financial freedom, make you money work for you while you sleep, and this can be done through investing. You can put your money in a time deposit or a bond wherein you’ll earn interest. You can also invest in stocks, real estate, or a business wherein the value of your investment grows; however, it’s best to note that investments are not guaranteed, and you can lose money as well. This is the importance of starting as soon as possible. The earlier you start investing, the more time you have to spread your risk through the years. The longer your investment, the less riskier they become.

The road to financial freedom

The road to financial freedom is not easy but nothing worth it ever comes without hardships and difficulties. What is important is you take the first step, be it opening a bank account or saving a small percent of your monthly salary. Once you take the first step, you’ll start building the discipline and the habit to continue making smart money choices, and before you know it, you’re already financially free.

As you experience financial freedom, always remember that money is only a tool, not the end goal. Be generous and always be a blessing to others. Wealth and the ability to create wealth comes from the Lord, and it is not for our own purpose, it is for His.

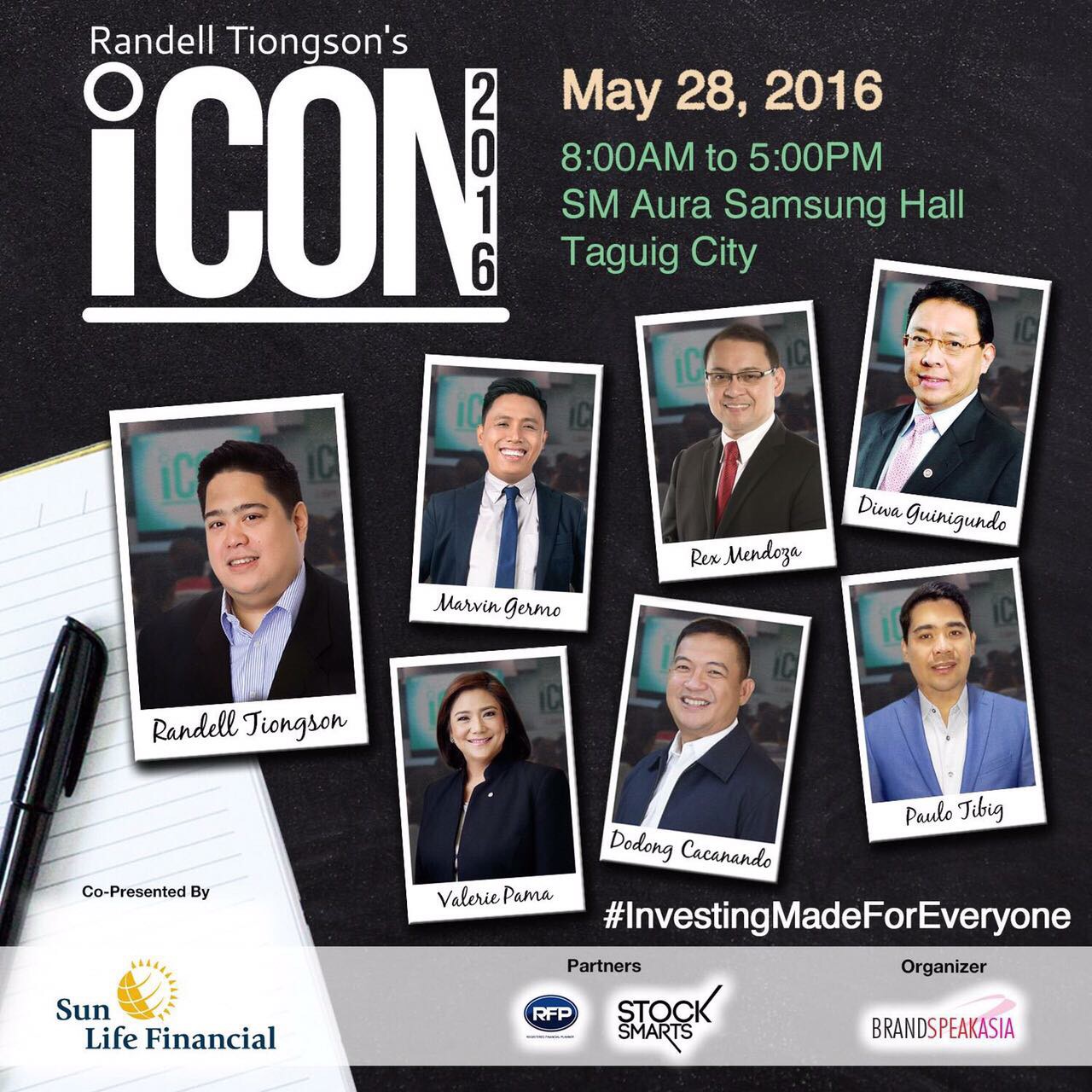

Join the biggest investment conference of the year – iCon2016! Visit www.iCon2016.info or contact 09266910126 for details.

Want a copy of my life-changing book No Nonsense Personal Finance: A Step by Step Guide? E-mail michael@randelltiongson.com on how you can order a copy.

Want to learn how to manage your finances better?

Register now and get a free copy of my e-book. Start your financial planning journey today!