5 Excuses Financially Savvy People Never Use

By Randell Tiongson on April 11th, 2016

Financial planning and management – it sounds like a daunting task. It’s already one thing to earn money, and it’s another to actively manage it and ensure you’re planning your finances properly.

You know that saving is important, and yet you’re always counting the days until payday because nothing’s left in your account anymore. You know that investing is a great opportunity to grow your money, and yet you keep holding it off because your salary is insufficient. You know you want to retire on a beach and drink cocktails or beer every day, and yet you haven’t started saving up for retirement – a time when you won’t be earning an income anymore.

Financial planning and management – it’s a daunting task, but everyone needs it. You might have the friend who seems like he has his finances in order. You may know of a colleague who manages to travel quarterly and yet doesn’t look like he’s starving himself to save. These people are the type to emulate; they’re financially savvy and have their finances in order.

Hoping to become one of them someday? You can start with changing your mindset and avoid making excuses. Here are 5 excuses financially savvy people never use:

I don’t know where to start

With the boom of the internet, information is more accessible at present day than it has ever been. A simple online search will give you the exact information you need. A person can spend hours on the internet each day. Why not allot a little bit of it to become productive?

The solution: Simple searches such ‘how to save my income’ or ‘what is a good investment’ are a great first step. The internet is a place that seems to have an answer for everything. Are you planning to open a bank account to stash your savings? Check the websites of different banks before going to local branches. Are you planning to apply for a mortgage to buy your first home? Use comparison websites, such as MoneyMax.ph, to learn a little more about home loans before you settle for one.

I’m busy

We all have 24 hours a day, but some people seem to get more things done than others. It’s about prioritization. When you say ‘I’m busy’, this means you’re not prioritizing that particular task.

The solution: To start, write down one financial goal you want to achieve per month. This can be tracking your expenses or saving X% of salary. After, write down specific steps you can do to achieve that goal. Now that you’ve written the steps, it’s time to prioritize them. If you want to save 10% of your salary, you would have to prioritize this over buying that artisan coffee or trying the new speakeasy bar that just opened up.

It’s difficult

Doing what is right is usually difficult to do. A specific example is buying a new pair of shoes. It’s much easier to do that to open a bank account. When you buy shoes, you have multiple payment options – cash, debit, or credit. When you open a bank account, you have to fill up and submit forms, IDS, and what have you. There’s no argument as to which one’s easier to do; however, what is easy isn’t always what’s right.

The solution: Start small so that action doesn’t seem so burdensome. Do you want to save a percentage of your salary? Why not start with saving 5% first? 5% of a Php 18,000 salary is only Php 900. Do you want to start investing? Why not read 500-word blogs about it first? The more you get the hang of a particular action, the less difficult it becomes.

I don’t have money for that yet

This is definitely one of the most common reasons why people forego financial planning and management. There’s a misconception that it takes huge amounts of many to start wealth-building.

The solution: As mentioned earlier, start small and shift your priorities. You can open an investment account with Php 5,000 or Php 10,000. The amount doesn’t matter at the start; what matters is you take the first step. Couple that with a changed mindset – prioritize saving over spending. If you put saving first before spending, you’re going to be saying, “I don’t have money to spend”. That’s much better than saying, “I don’t have money to save”.

Y.O.L.O.

You only live once. So why save for the future and live a miserable present? However, you can find a balance. YOLO doesn’t mean you quit your job, travel the world, and figure it you. Why not travel and work at the same time? You can save your vacation leaves to travel or take part-time work in whichever country you’re in.

The solution: Find the balance between fun and practical. This can be hiking during the weekend to explore the outdoors instead of spending it in the mall. This can be having a potluck dinner with friends instead of dining in a restaurant with outrageous mark-ups. The key is to find a balance. Be practical and have fun at the same time. Save for your future self without sacrificing your present self.

Financial planning and management – it’s a daunting task, but everyone needs it. Taking the first step is always the hardest, so why no start by changing your mindset, slowly but surely. Say ‘goodbye’ to the excuses above, and challenge yourself to reach your money goals. Sooner or later, you couldn’t believe the excuses you used to say in the past because you’ve already gotten used to financial planning and management that it becomes easy and automatic.

———

It’s time to be an empowered investor! Join the biggest investment conference of the year – iCon2016 this May 28, 2016

Visit www.icon2016.info for details.

Investing on an election year?

By Randell Tiongson on April 6th, 2016

QUESTION: Good day, Sir Randell! I’m Mara, a 27-year-old who started investing a couple of years ago. Right now, my portfolio is a mix of red and green. Right now, my gains are more than my losses, so whew. I’ve been told that stocks are among the best tools for investing, but with the looming elections and with 2016 considered to be a slow year for world economies, I’m conflicted. Should I put my money in cash first and stop investing during this election year? Your help would be greatly appreciated. Thank you po, sir Randell!—Mara via e-mail

Answer: Hello Mara! Congratulations on the performance of your stocks. Where most people are suffering from the downturn, you managed to gain rather than lose. However, I understand your dilemma. The next President is sure to have a strong influence on sectors and industries which will be given focus and drive the economy in the coming years. How do we pick which company stocks to buy during this election year? Or should we even invest at all? Here are my thoughts that may help you decide if you should invest this 2016:

Make a decision that sticks to your investment strategy and objective

In my book No Non-Sense Personal Finance, one of the investing guidelines I put is to know your objective for investing. Objectives will determine nearly every action we make with regards to finance.

What is your investment intended for? For retirement? For higher education? In addition, also determine your strategy in relation to your objective. Are you a long-term or short-term investor? If you’re a long-term investor with over 30 years until retirement, the upcoming elections will have lesser influence on the performance of your investment than if you were a short-term investor.

If you’re a short term investor, it’s best to sit and wait until the country has a new President. You can form your stock picks by focusing on companies in industries which the next President plans to focus on, be it mining, real estate, or infrastructure development. If you’re a long term investor, remember that there are companies that will stand the test of time. From banking to water and electricity services, it’s hard to imagine a Philippines without banks and other services.

The Philippines is a fundamentally sound economy

Last Feb. 2, I attended the Eaglewatch 2016 Elections Briefing hosted by Ateneo de Manila University (ADMU).

The first speaker, Dr. Alvin Ang, gave an analysis of the economic landscape of the Philippines and his projections for this 2016. He covered the performances of remittances (which are tapering off), the BPO industry (which will exceed OFW earnings), and real estate (high-end developments declined while mid-income housing increased) among others.

During this economic briefing, Dr. Ang enumerated the different factors that make the Philippines a fundamentally sound and stable economy. Despite the real estate market in a general decline from last year, there are different segments that experienced triple- and double-digit growth—commercial subdivisions at 39.81 percent, mid-income housing at 56.58 percent, and socialized housing at 101.23 percent.

Also, the BPO industry is expected to grow and will exceed OFW remittance earnings in the coming years and the debt to GDP ratio (at 45.4 percent as of Jan 2016) is much lower than other world economies.

Looking deeper (at the details) shows that the country is sound and stable economically.

In relation to investing during an election year, you may be feeling nervous. You just cannot lose your hard-earned money. But remember, the Philippines is a fundamentally sound and stable economy.

What will you do?

After reading the points above, you may now have a clearer picture of what you will do this election period. Depending on your investment objective and strategy, you now know whether or not you should invest right now and which stocks to put your money into.

On a larger scale, looking at the Philippine economy and the performances of different sectors will help you determine further where to invest and not to invest in. Happy 2016 to you, Mara!

The biggest investment conference is back! Join me, BSP Deputy Governor Diwa Guinigudo, Marvin Germo, Paulo TIbig, Rex Mendoza and Reina Pama iCon2016 this May 28, 2016 at the Samsung Hall of SM Aura.

Visit www.bit.ly/GO_ICON2016 for details and registration.

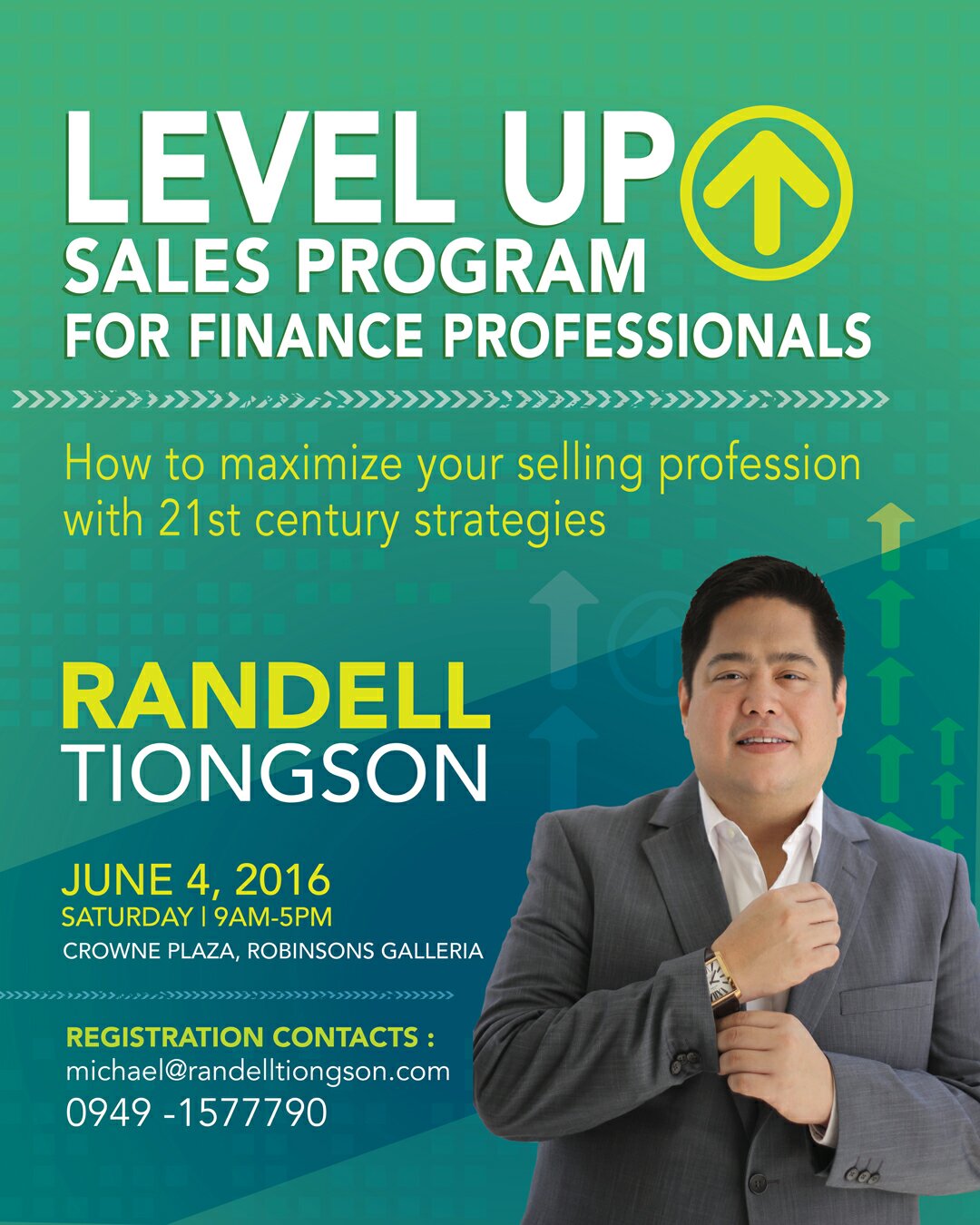

Level Up Sales Program

By Randell Tiongson on April 3rd, 2016

I have often been asked for advise and guidance as to how to properly & effectively succeed in the sales profession– specifically in the industry of finance and investments. My answer? You should have the proper knowledge and develop the right skills as a foundation.

Many people believe that selling is an art and it is limited to those who are very good in soft-skills. While I agree that soft-skills are important for the sales profession, the science of proper selling is just as important, if not even more important.

If you are in the selling profession, specifically on financial services and investments such as insurance, mutual funds, UITF, stocks, real estate and other related industries and you feel that it’s time to “level-up”, you should attend my upcoming program: Level Up Sales Program for Finance Professionals.

On June 4, 2016, I will be running a new program that I designed to help those in the sales profession to level-up and become even more successful in a very challenging field. The whole day program will be held at the Crowne Plaza, Robinson’s Galleria.

The comprehensive program will cover 4 areas which I believe are 21st century strategies to thrive in sales:

- Buying Cycle

- Selling Cycle

- Behavioral Finance

- Powerful Sales Presentations

This program will incorporate effective theories validated by my 28 years of experience in the financial services industry.

Level Up Sales Program will only have a limited seating capacity to make it effective so make sure you register immediately.

The learning fee of the program is only P 7,500.00 — an investment that will have exponential returns.

If you will register before April 15, 2016, you can avail my early bird rate of only P 5,000.00

Follow the simples steps to secure your slot

- Deposit the training fee to my BPI Savings Account #0249-1113-09

- Send the photo of the deposit or transaction slip to michael@randelltiongson.com along with the following additional information:

- Full name

- Contact details (email and mobile phone)

- Company Affiliation

- Brief job description

- Years of experience

See you at the program!