What are BONDS?

By Randell Tiongson on September 19th, 2012

With all the attention the stock market gets latelty, you would think that they would be the bulk of investments being made in the Philippines, right? Not really. Bulk of investments in this country are credit instruments like Bonds. I guess it’s high time to post about fixed income or bonds in this blog.

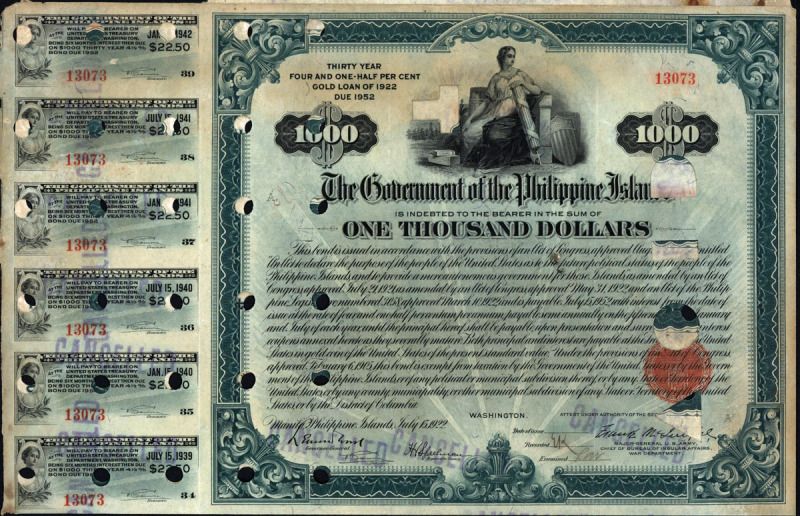

What are bonds? Bonds are contracts in which an investor lends money to a borrower. As compensation for receiving the money, the borrower agrees to pay interest, often twice a year and generally of a fixed amount. The borrower also agrees to repay a stated sum at the end of a fixed period. The date that the loan is to be repaid is called the maturity date.

Bonds issued by a sovereign state are known as Government Securities. It is usually considered zero or minimal risk because the government backs the indebtedness. In the Philippines investment scenarios, majority of fixed income investments are done through government securities. However, there are some investment grade bonds issued by top corporations such as PLDT, Ayala Corp., San Miguel Corp., SM, etc. Obviously, the risk associated with corporate bonds are higher than those issued by the government, hence one can expect higher yields from corporate bonds.

Bonds of high-quality companies are considered safer than most of investments for the following reasons:

1. The annual income to be received is generally fixed in advance

2. The contracted – for loan principal is likely to be repaid in full at the stated due. In the even financial difficulties, the borrower will have to comply with the terms of the contract. Interest and principal will be repaid on time or the company will be faced with bankruptcy. Should bankruptcy occur, bondholders have priority in receiving the proceeds from liquidation of business assets and are therefore repaid before stockholders receive any material proceeds.

In general, Bonds are:

• Notes and bonds are debt securities issued by borrowers. These debt securities are also referred to as fixed income securities since they give coupon or interest payment on a regular or a fixed basis. Basically, these are “IOUs”.

• Technically, the term “bond” is used for securities with tenors of more than 10 years while “note” is used for securities with tenors of less than 10 years.

• Treasury Bills – Government Securities traded at discount to FV, One year or less

• Commercial Papers –Similar to T-Bills, except as to ISSUER

Bond prices will vary throughout its lifetime and are largely dictated by market prices. Generally, Bond prices are affected by supply and demand, prevailing interest rates, credit standing of the issuer, the economy and other factors.

If Bonds are deemed as fixed-income securities, why do prices fluctuate? Basically, bond prices fluctuate because they could be traded in the secondary market, which ultimately determines the value of a bond based on supply and demand & market forces.

You can invest directly in bonds by buying them or through managed funds that invests primarily in bonds like “Bond Funds”.

Hope this helps!

Catch me at No Nonsense Seminar on Finance: How to Invest for the Future, presented by Sun Life Prosperity Funds. It’s my investment seminar and it will be held on Sept. 22, 2012 at the Legend Villas, Pioneer St., Mandaluyong City. For inquiries, send email to vlqmagalong@gmail.com Details HERE

Caution!!! Debt is Looming Ahead by Malloy

By Randell Tiongson on September 28th, 2009

This is a written by my on-line friend, Malloy. He is an OFW based in the Middle East. Originally posted at his Multiply Site. Very good read!

—————————–

God’s perfect plan for His people is to be debt-free. As we are serving a jealous God, He only wants His people to serve nothing else except Him only. For how can one serve only Him if one is in shackle of indebtedness.

God’s perfect plan for His people is to be debt-free. As we are serving a jealous God, He only wants His people to serve nothing else except Him only. For how can one serve only Him if one is in shackle of indebtedness.

When a Christian confess with their mouth, and believing in their heart Jesus Christ as their personal Lord and Savior, it is tantamount to accepting God’s offer of our redemption from the slavery to sin. In effect, the ownership of a Christian’s life has changed hands from the prince of darkness and sin to God. As a new master, the slave is ought to serve Him alone.

Jesus even warned us sternly when He says that we can not serve both God and mammon. For how can you spiritually worship the master and sovereign God if you are financially in trouble with indebtedness.

Nevertheless, God is not short of giving us reminders of the dangers of debts. He provided us a number of practical principles and guides, through the Bible on how and why indebtedness is dangerous.

In this article, I am herewith giving three, as I call it the 3S. Here the are:

1. Speculates the future (Prov. 27:1)

2. Synthetic Decision (Prov. 21:5)

3. Stops God’s will (wisdom and power) to work (2 Chron 16:9)

When one entered into a loan agreement, one commits himself to payments over a period of time, hence presuming that nothing untoward will happen such as loss employment and other unexpected expenses. Prov. 27:1 sternly warns us not to boast of the future for no one knows what tomorrow may bring.

A lot of expatriates in the UAE having hundreds of Dirhams of indebtedness got into trouble with banks and financial institutions because of termination from employment.

Secondly, synthetic rather than real life decisions are being made because of borrowing. This applies to installment purchases of an item. Because borrowing, one may decide to purchase based on whether he could afford the monthly installment rather than the total cost of such an item. Entering into a debt transaction makes it easy to say yes to low monthly installment s while ignoring the real cost of the item.

And lastly, debt could stop wisdom and power of God working in us. One may earnestly pray for some material blessing, but could not wait God to answer the prayers. Does not God taught us that patience is one of the virtues a Christian must posses? Resorting to debt in acquiring the item prayed for is like taking in advance the answer to your prayer, when you are not sure as yet as to how God will answer your prayer.

Presented herein are only 3 of those numerous teachings of the Bible in regards handling our finances and the dangers of debt. Read your Bible, take heed of its teachings, be obedient. For He who is obedient will not borrow, but will lend. He will be the head and not the tail, as the God promised.

Dave Ramsey says “Debt is not a tool”

By Randell Tiongson on September 17th, 2009

Many of us grew up with the notion that debt is part of our lives and will always be here to stay. I even here people say that “walang mayaman na walang utang” … obviously, that’s not really true. I know many rich people and most of them have no debts, personal or business.

Here’s what Dave Ramsey says…

“Debt is not a tool!”

Myth: Deb is a tool and should be use to create prosperity.

Truth: Debt adds considerable risk, most often doesn’t bring prosperity, and isn’t used by wealthy people nearly as much as we are led to believe.